FAFSA •

November 15, 2022

Do you have to pay back FAFSA?

The FAFSA allows you to qualify for financial aid to help pay for college, but you may have to pay back some of the money you receive.

Getting enough financial aid to pay for your college education is one thing, but it’s also important to remember that you’ll likely need to repay some of that money later.

The problem is knowing which money is yours to use—and which you’ll eventually need to pay back.

Thankfully, it’s pretty easy to figure out which types of student aid fall into which of those buckets.

In this article, we'll explain what the FAFSA is and what forms of financial aid you can get through it, plus the kinds of aid you need to pay back and the ones you don’t.

We'll also discuss when you’ll need to start paying back financial aid and how long you have to do it.

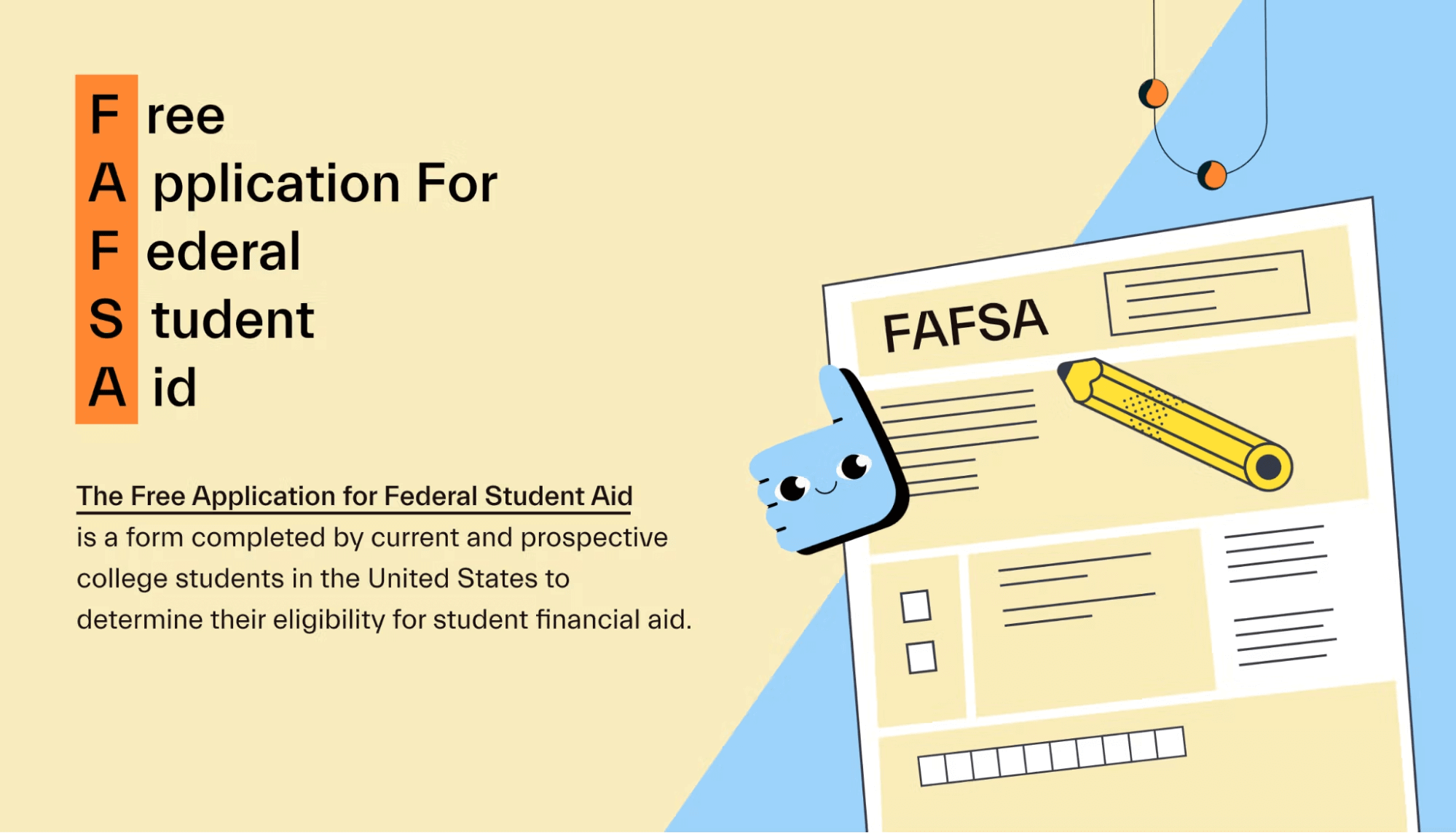

A quick primer: What is the FAFSA?

The FAFSA—short for Free Application for Federal Student Aid—is a form that college students complete each year to apply for financial aid to help pay for undergraduate, graduate, and professional school.

Usually, you have to complete the FAFSA to qualify for federal financial aid, such as grants, federal work-study, and federal student loans. The form is free to fill out and can help you get tens of thousands of dollars in aid to help pay for college!

The information you share on your FAFSA helps your school’s financial aid department determine what aid you’re eligible for and put together your financial aid package.

First, based on your and your family’s income and assets that you’ll share on your FAFSA, the school will find your expected family contribution (EFC). This is the amount of money they expect you and your family to contribute to your education, even if you and your family don’t actually put that much towards college costs.

Then, based on your school’s cost of attendance (COA), the financial aid office will figure out how much aid is necessary to fill the gap.

Finally, each school you apply to will send you a financial aid award letter detailing its COA and all of the aid you’re eligible to get if you attend that school.

Some types of financial aid are need-based, meaning you only qualify if your FAFSA shows your EFC isn’t enough to cover the cost of your education. Those types of aid include the Federal Pell Grant, subsidized student loans, and the federal work-study program.

Other types of aid are non-need-based, meaning they aren’t impacted by the information you share on your FAFSA. Those types of aid include unsubsidized loans, PLUS loans, merit scholarships, and the TEACH Grant.

Want help navigating the FAFSA, financial aid, scholarships, and more?

Mos is a money app that helps students save, earn, and manage their money while in college. With Mos, students can get 1-on-1 access to a financial aid pro, unlimited essay editing, hand-picked scholarship opportunities, and much more. Connect with a Mos financial aid advisor today!

Do you have to pay back the money you get from FAFSA?

Depending on the type of financial aid you qualify for by filling out the FAFSA, you may need to repay some money. Before accepting any financial aid, be sure you know if you’ll have to pay it back and when.

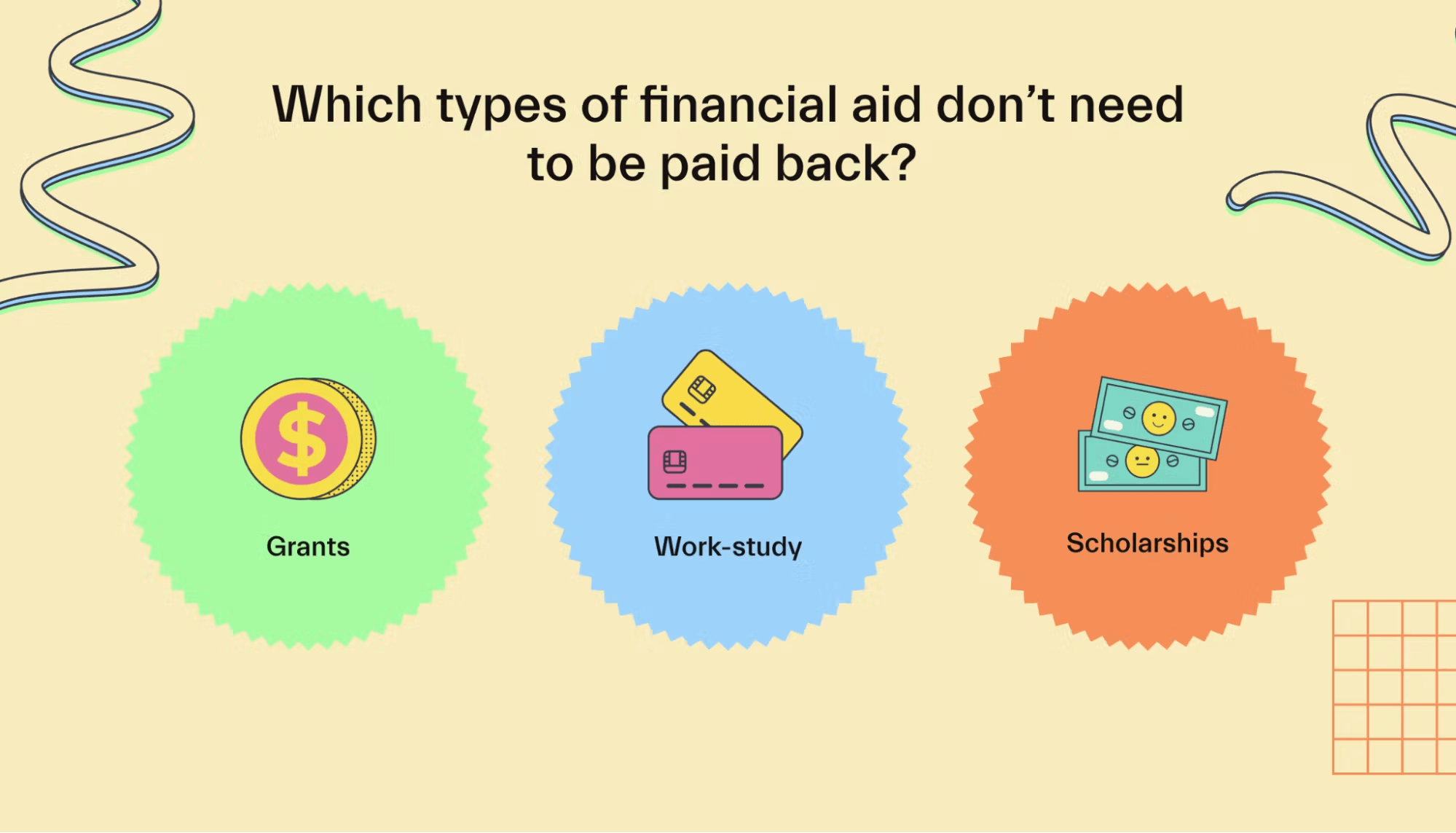

Which types of financial aid don’t need to be paid back?

The good news is that there are plenty of college financial aid dollars that you won’t have to repay!

These aid sources are basically free money. Therefore, you should try to get as much of this aid as possible—it’ll help you minimize student loan debt after graduating.

One type of aid that you won’t usually have to pay back is grants. They’re a type of free aid that comes from the federal government, state governments, and some individual schools and private organizations.

The most common federal grant is the Pell Grant, which is available to undergraduate students who have financial need. Other federal grants include:

Federal Supplemental Educational Opportunity Grant (FSEOG) for undergraduate students with exceptional financial need

Iraq and Afghanistan Service Grant for students whose parent or guardian died because of military service in Iraq or Afghanistan

Teacher Education Assistance for College and Higher Education (TEACH) Grant for aspiring teachers who teach in a low-income school or high-need field

It’s worth noting that while you generally don’t have to repay federal grants, there are a few exceptions. You’ll have to pay back your grant money if you fail to keep your eligibility.

This could happen if you withdraw from your program, switch from full-time to part-time, receive an outside scholarship that changes your financial need, or receive a TEACH Grant but don’t teach in a qualifying school.

If you have to pay back grant money, you’ll have just 45 days to do so after your school notifies you that you need to repay it.

If the Federal Pell Grant isn’t enough, or you aren’t awarded it, you can then look to your state and local governments. For example, students resident in New York that fill out the FAFSA also have the NYS Tuition Assistance Program available to them.

After that, try private and non-profit organizations for more grant opportunities.

Another type of federal aid you won’t have to pay back is money you earn from a work-study job.

The federal work-study program provides part-time or full-time employment (depending on your enrollment status) to undergraduate and graduate students.

A work-study job is just like any other where you’re paid for your work, usually on an hourly basis. Wages in these jobs start at minimum wage but can be higher for more specialized roles. Your hours are capped, so you can’t work as much as you want. However, your employer and financial aid office will do their best to make sure your hours don’t conflict with your class schedule.

As far as the type of work you can do in a work-study job, it varies widely. Often, work-study jobs are available on campus. You can also find off-campus jobs at non-profit organizations, public agencies, and other places that perform work in the public interest.

According to the Department of Education’s Federal Student Aid Office, the work-study program tries to place you in a job relevant to your major or civic education wherever possible. For example, if you’re an accounting major, you may get a role in your school’s accounting office.

Just like any other type of earned income, you’re paid work-study wages in exchange for the work you provide, and so that you won’t have to pay the money back. Wages are paid to you directly for you to use on college costs. However, you can request that your school put that money into your bank account or directly toward college costs, like tuition and fees.

Scholarships are another type of free financial aid that you won’t have to pay back.

While the federal government doesn’t offer scholarships, many schools offer them, and some are based on the information you provide on your FAFSA. Beyond that, there are nearly endless numbers of scholarships available through private organizations, and you can find these by searching online or using an app like Mos.

Some, like the Courage to Grow Scholarship, have quick and easy applications that involve no more than a few questions. Others, like the Ron Brown scholarship, are much more exclusive but offer larger amounts of aid to those who qualify.

While you generally don’t have to repay scholarships, some organizations may have rules about what you can use the money for. Be sure you read the requirements, so you don’t end up having to pay the money back.

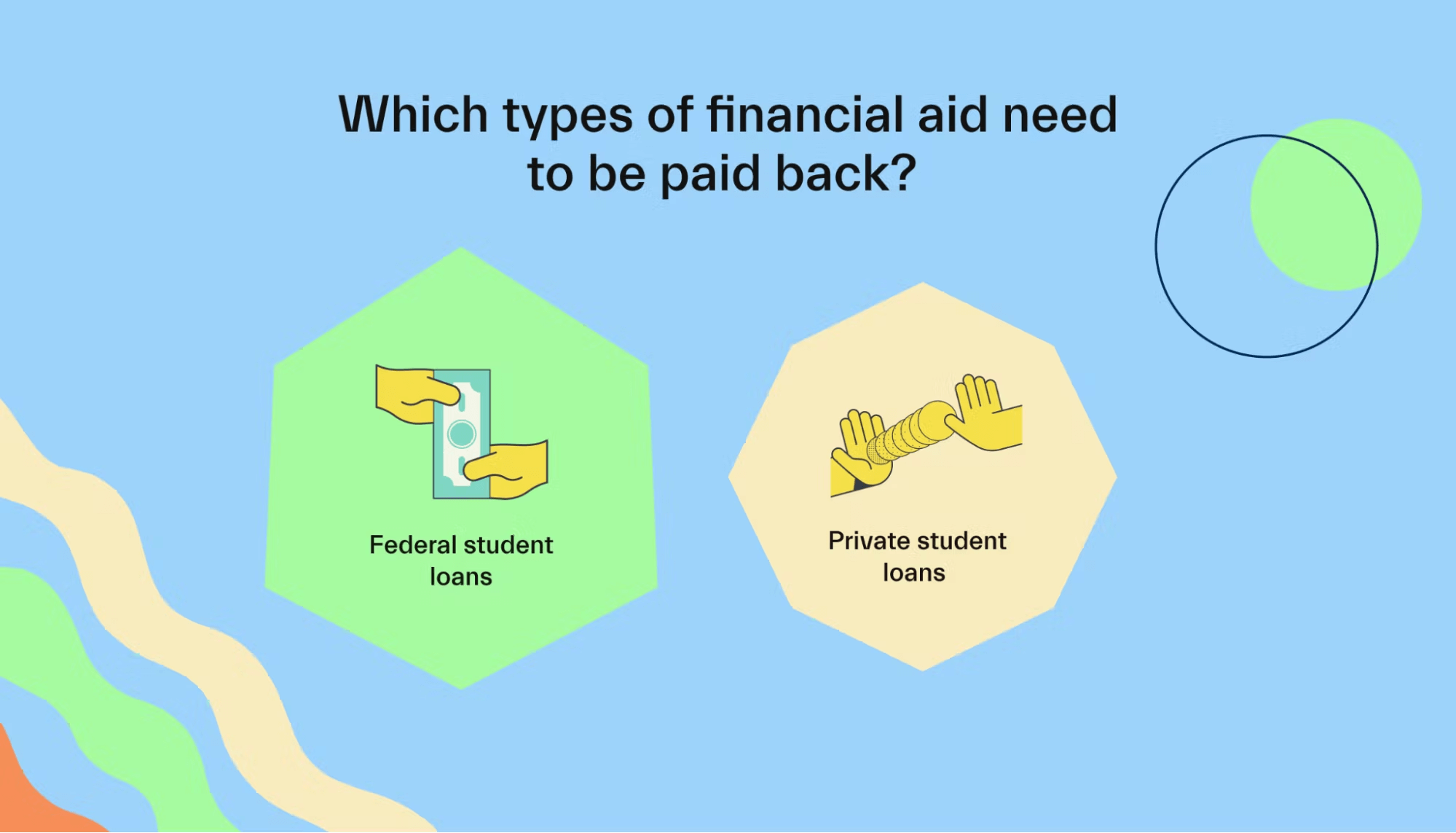

Which types of financial aid do you need to pay back?

While there are plenty of types of financial aid money you qualify for with the FAFSA that you don’t have to repay, there are some types that you do.

Therefore, make sure to exhaust all of your “free money”—grants, scholarships, and so on—before using the financial aid you have to repay.

First, as we discussed previously, you may have to repay grant money if you no longer meet the eligibility requirements. If this happens, your school will let you know, and you’ll have to either repay the money or enter into a payment plan right away.

Other than that, the most common type of financial aid that you have to repay is a student loan.

There are four types of federal student loans you can qualify for with the FAFSA:

Direct subsidized loans: For undergraduate students who demonstrate financial need. These loans don’t build up interest while you’re in school.

Direct unsubsidized loans: For undergraduate, graduate, and professional students regardless of financial need. These loans build up interest while you’re in school.

Direct PLUS loans: For graduate or professional students and the parents of undergraduate students.

Direct consolidation loans: For all people who borrow federal money. These allow you to combine multiple student loans into one.

The differences between these direct loan types are important because each has different repayment terms. We’ll discuss those later.

While federal student loans are the only ones whose eligibility is based on the FAFSA, it’s still worth mentioning private student loans.

Many private lenders offer these loan money to students who don’t qualify for federal loans, don’t qualify for enough money through federal loans, or simply prefer not to borrow a federal loan.

Just like federal student loans, private student loans will eventually have to be repaid. But because the lender is a private financial institution instead of the federal government, the repayment terms will be a bit different.

How FAFSA repayment works

If you borrowed student loans after completing your FAFSA, then you’ll have to repay them. Below, we’ll discuss when and how you can repay your federal student loan.

When do students have to start paying back financial aid?

You’ll have to start making student loan payments after you leave school—whether it’s because you graduated or for another reason—or if you drop below part-time enrollment.

You’ll generally get a 6-month grace period before you have to start making payments. You can use this grace period to get to know your loan servicer, figure out what your monthly payment will be, and prepare to fit it into your budget.

It’s important to note that PLUS loans don’t have a grace period.

If you borrowed a Grad PLUS loan or your parents took out a Parent PLUS Loan, repayment may start right away after graduation.

However, the federal government allows Grad Plus borrowers an automatic 6-month deferment, and Parent PLUS borrowers can request a 6-month deferment.

How does student loan repayment work?

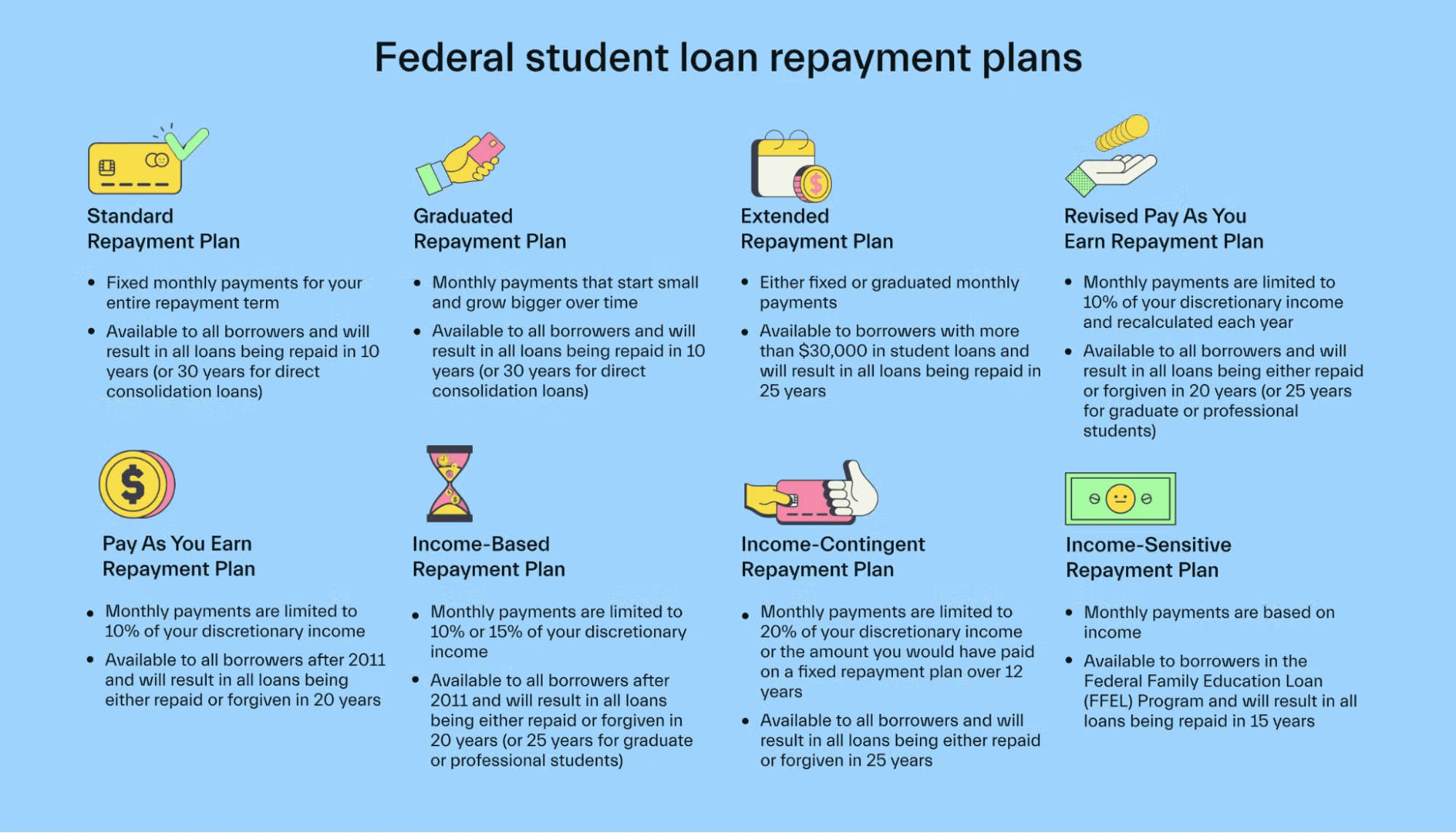

When you leave school and have to start making student loan payments, you’ll have several repayment plans to choose from. The repayment plan options currently available are:

Standard Repayment Plan: Fixed monthly payments for your entire repayment term. Available to all borrowers and will result in all loans being repaid in 10 years (or 30 years for direct consolidation loans).

Graduated Repayment Plan: Monthly payments that start small and grow bigger over time. Available to all borrowers and will result in all loans being repaid in 10 years (or 30 years for direct consolidation loans).

Extended Repayment Plan: Either fixed or graduated (meaning the payment will become bigger) monthly payments. Available to borrowers with more than $30,000 in student loans and will result in all loans being repaid in 25 years.

Revised Pay As You Earn Repayment Plan: Monthly payments are limited to 10% of your discretionary income and recalculated each year. Available to all borrowers and will result in all loans being either repaid or forgiven in 20 years (or 25 years for graduate or professional students).

Pay As You Earn Repayment Plan: Monthly payments are limited to 10% of your discretionary income (but not more than your payment would be on the standard repayment plan) and recalculated each year. Available to all borrowers after 2011 and will result in all loans being either repaid or forgiven in 20 years.

Income-Based Repayment Plan: Monthly payments are limited to 10% or 15% of your discretionary income (but not more than your payment would be on the standard repayment plan) and recalculated each year. Available to borrowers who have a lot of student loan debt compared to their income and will result in all loans being either repaid or forgiven in 20 years (or 25 years for graduate or professional students).

Income-Contingent Repayment Plan: Monthly payments are limited to 20% of your discretionary income or the amount you would have paid on a fixed repayment plan over 12 years. Available to all borrowers and will result in all loans being either repaid or forgiven in 25 years.

Income-Sensitive Repayment Plan: Monthly payments are based on income. Available to borrowers in the Federal Family Education Loan (FFEL) Program and will result in all loans being repaid in 15 years.

The Department of Education website has a loan simulator you can use to figure out which payment plans you might be eligible for and how much your monthly payment will be with each one.

Private student loan repayment

Private loans aren’t from the federal government and aren’t based on your FAFSA, but it’s still important to understand how repayment works.

These types of loans come from traditional lenders, such as banks, credit unions, and online loan providers.

Many schools don’t require you to repay your private student loan while you’re in school, and some offer a grace period after you leave school, just like the federal government does.

You should keep in mind, though, that these aren’t hard and fast rules, so you should check with your lender to see if that’s the case for you.

While private lenders generally don’t require you to make payments while you’re in school, your loans will typically build up interest. This means that the amount you owe after graduation will be more than what you borrowed unless you make interest payments while you’re in school.

Private lenders may have stricter repayment terms, such as set monthly payments and loan terms that aren’t related to your income or ability to pay.

Private loans may be harder to qualify for as well. Unlike federal loans, many private lenders will want to see a good credit score before approving you. Chances are you don’t have much credit history yet, so you may need a parent or guardian to cosign a private loan.

Additionally, many private lenders don’t offer loan forgiveness programs except for in rare, extreme circumstances. Similarly, deferment and forbearance availability can vary by individual lender.

Because of these disadvantages, it’s a good idea to exhaust all federal loan options before looking for private loans.

But ultimately, private lenders want you to repay, or they lose money. So they may work with you to set up a plan that keeps you on track and helps you pay off your debt.

Can FAFSA loan debt be forgiven or canceled?

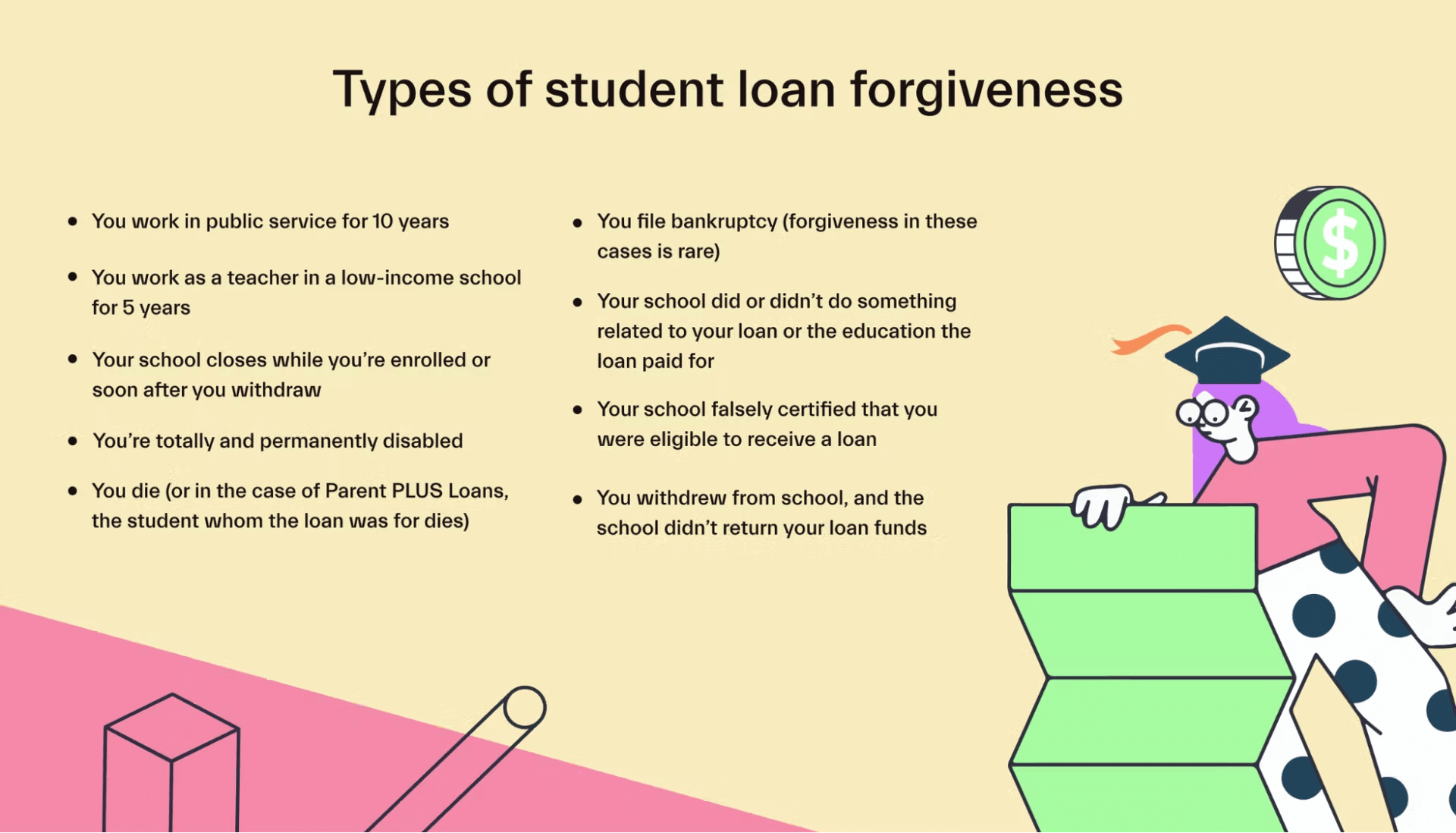

Though federal student loans generally have to be repaid, there are some exceptions! The federal government offers select situations where your loan can be either forgiven or canceled. Those situations include:

You work in public service for 10 years

You work as a teacher in a low-income school for 5 years

Your school closes while you’re enrolled or soon after you withdraw

You’re totally and permanently disabled

You die (or in the case of Parent PLUS Loans, the student whom the loan was for dies)

You file bankruptcy (forgiveness in these cases is rare)

Your school misled you or engaged in misconduct related to your loan or your education

Your school falsely certified that you were eligible to receive a loan

You withdrew from school, and the school didn’t return your loan funds

You can contact your loan servicer if you think you might be eligible for student loan forgiveness or cancellation because of one of these circumstances.

Conclusion

The financial aid money you can get when you complete the FAFSA each year can go a long way in helping you to pay for college costs. But just like any other big financial decision, it’s important that you fully understand what you’re getting yourself into before accepting your financial aid package.

Luckily, there are plenty of types of financial aid, like grants and work-study, that you don’t have to repay! But if you borrowed student loans after completing the FAFSA, then you’ll have to pay that money back.

Need a hand completing your FAFSA and qualifying for more financial aid? Connect with a Mos expert financial aid advisor today.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you