Budgeting •

October 28, 2022

6 creative ways to pay off student loans

Read this guide from Mos to learn about creative ways to pay off student loans.

Nobody likes to have the feeling of debt hanging over their head.

Taking on student loans might’ve been the only way that you could pay for college. But that doesn’t mean that you have to be stuck paying off your debt for the next 20 years.

Putting extra money toward paying off your student loans can help you save thousands of dollars in interest and get you out of debt faster!

This article will explain 6 creative ways to pay off student loans, ways that you can earn extra income, and how people with a low income can reduce their student loans.

Why pay off student loans quickly?

In a perfect world, you could pay for college using just scholarships or grants—which would mean you don’t have to pay anything back after you graduate.

Sadly, most people don’t live in a perfect world, so they’ve got to establish a funding mix using a combination of loans, grants, and scholarships.

But it takes the average borrower 20 years to pay back their student loan debt! What’s more, a typical US student loan builds up $26,000 in interest over that time.

Translation: if you can afford to pay back your student loans early, it’ll literally save you thousands of dollars.

It’ll also drastically lower your debt-to-income ratio.

For reference, a debt-to-income ratio is just the part of your gross monthly income that you can apply toward making monthly debt payments.

This ratio is pretty important because lenders use it to decide whether or not they want to extend you credit.

For example, if you need to take out a loan for a new car, a lender would want to look at your debt-to-income ratio to make sure you can afford to make the monthly payments on that car.

Assuming you’re in a position to pay back your student loan early, you’ll also benefit from the fact that there aren’t usually penalties for paying your student loan back quickly.

Some lenders build clauses into loan agreements that penalize you for repaying your loan early. But you aren’t going to get that with a federal loan—and so if you can clear your loan balance early, you’re only going to save money.

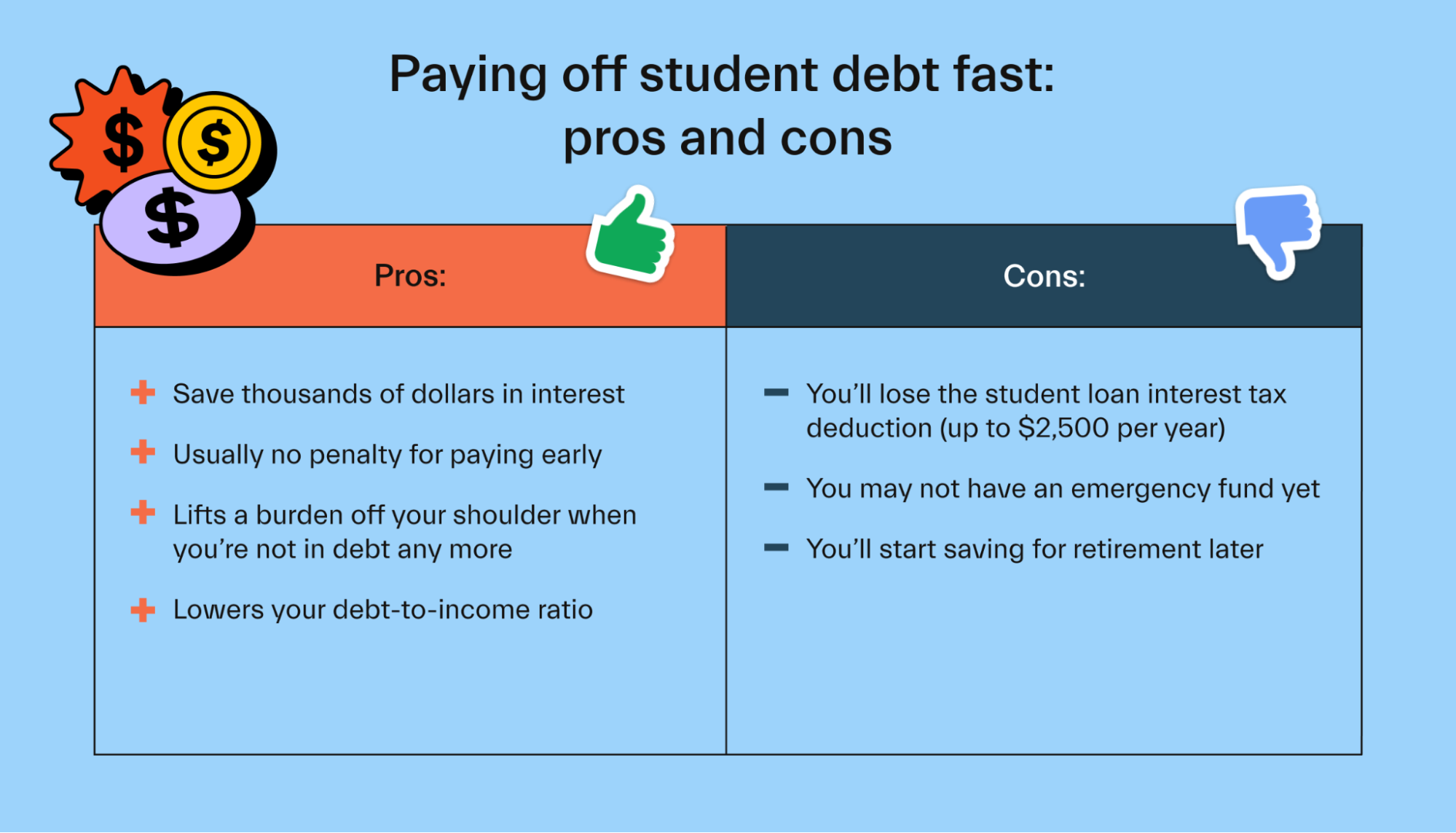

Are there any downsides to paying off student loans quickly?

Generally speaking, paying off your student loans quickly is a good thing. That being said, there are a couple of small drawbacks that you should think about before clearing your loan balance.

First, you’ll miss out on a student loan tax deduction.

You’re allowed to deduct up to $2,500 in interest each year off your tax return. After you’ve repaid your loan, you won’t be paying off interest—which means you can’t claim interest payments on your tax return.

Another thing you should consider when paying back your student loans quickly is that you’re going to have to make sacrifices elsewhere.

For example, you may need to empty your savings account to get your loan paid off. That means you aren’t going to have an emergency fund in case you run into any big and unexpected expenses.

A solution for this might be to make sure you’ve saved a reasonable amount of money and set it aside before you start paying off your student loans early.

Finally, repaying a student loan early could prevent you from saving early for retirement. That might not seem like a big deal when you’re in your 20s, but it’s something you’ve got to consider.

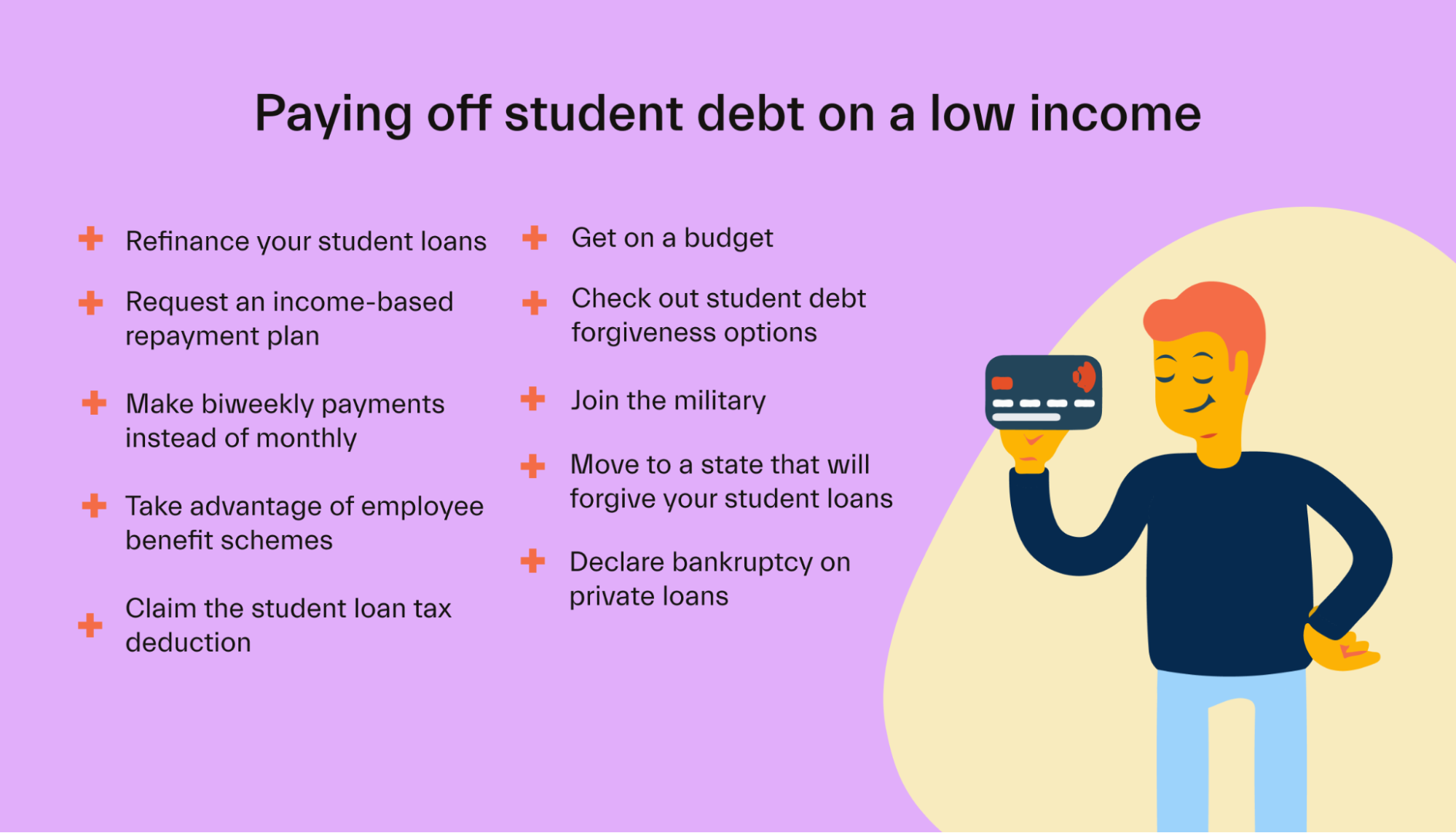

10 ways to pay off student loans on a low income

Let’s face it: most college graduates don’t start earning six figures the day after they move out of the dorms.

Generally speaking, a lot of students join the world of work on a relatively low income—and when you don’t have a lot of disposable income, it can make repaying student loans a bit trickier.

To help you get started, we’ll break down 10 methods to help you repay your student loans.

1. Refinance your student loans

If you’re having trouble paying your loans back on your current salary, one option is to refinance your student loans.

The first step towards refinancing your student loan is to get in touch with your loan provider.

Generally speaking, you’ll be able to transfer your debt to a new account. This transfer could be to a different loan type with the same bank or to a different bank.

Either way, the end result of refinancing a student loan is that you should be able to secure a lower interest rate or repayment terms that you can afford easier. That will enable you to pay back your loans without having to put in extra cash.

2. Request an income-based repayment plan

If you’ve taken out a federal student loan and are having trouble making monthly payments, there are a few government programs designed to help.

Just like refinancing a loan, the first step to request an income-based repayment plan is to contact your loan servicer as quickly as you can. Depending on your personal circumstances, you may then be offered 1 of 4 income-based repayment plans:

Income-based repayment (IBR) plan

Income-contingent repayment (ICR) plan

Pay as you earn (PAYE) repayment plan

Revised pay as you earn (REPAYE) plan

An IBR plan is a federal student loan repayment method that figures out your loan payments by calculating 10% of your discretionary income.

An ICR plan is similar to an IBR plan. But ICR plans work out your discretionary income using the adjusted gross income (AGI) on your federal income tax return. You’ll then normally be asked to repay 20% of your discretionary income.

PAYE looks at your AGI, too. But instead of 20%, PAYE plans typically ask you to repay loans using 10% of your disposable income.

REPAYE loans work pretty much the same as PAYE plans. The only major difference is that the repayment terms are usually longer.

3. Make biweekly payments instead of monthly

Another solution to pay off your loans on a low income is to switch from a monthly payment plan to a biweekly one.

By paying smaller amounts of money on a more frequent basis, you’ll be able to keep up with your repayment schedule—but it should also make life simpler for you in terms of budgeting out the rest of your life using the rest of your discretionary income.

4. Take advantage of employee benefit schemes

Some companies offer student loan repayment programs as an employee benefit. These schemes can help you pay off your loan faster.

Ask your employer whether they offer any student loan repayment programs.

5. Claim the student loan tax deduction

If you’re making student loan payments, you should be claiming the student loan tax deduction.

The IRS lets you deduct up to $2,500 worth the interest paid on a loan for higher education. That means paying your student loans will actually save you a bit of money on your IRS tax return—so it’d be silly not to claim it.

6. Get on a budget

One of the most important things you should do when trying to pay back a loan on a low income is to get on a budget.

Try to cut back on unnecessary expenses like eating out or going out for coffee all the time. Think hard about what you can actually afford, and factor all of your debt obligations and necessary expenses against your monthly income.

7. Check out student debt forgiveness options

If you’ve taken out a federal student loan, you may be eligible for one of several student loan forgiveness programs.

These programs are only available to certain eligible graduates.

For example, the Public Service Loan Forgiveness is available for those employed by government or non-profit organizations after they’ve made 120 qualifying payments.

There’s also the Teacher Loan Forgiveness program for teachers that have completed 5 consecutive years teaching in a low-income school.

There are a few other options worth checking out on the Federal Student Aid website.

8. Join the military

If you decide to join the military, there are a number of generous loan forgiveness schemes you might be eligible for.

The Navy loan repayment program offers up to $65,000 in loan forgiveness if you serve at least 3years in your first enlistment.

The Air Force College Loan Repayment Program can pay up to $10,000 of your student loan balance.

If you enlist as an active-duty health professional, you could be eligible to receive $40,000 a year for up to 3 years toward your student loan debt.

You also don’t need to pay bills while you’re enlisted, which means more of your salary could go toward paying down debt.

9. Move to a state that will forgive your student loans

It’s worth noting there are some US states that have their own unique loan forgiveness schemes.

For example, Kansas has 77 counties designated as "rural opportunity zones." If you move to any of those areas, the state will forgive $3,000 of student loans every year for 5 years. That means that in just 5 years, you could reduce your student loans by $15,000, plus save thousands in interest.

10. Declare bankruptcy on private loans

If you genuinely can’t afford to make any loan payments and have no options left, you could declare bankruptcy and try to have your student loans discharged.

Getting student loans discharged through bankruptcy requires a couple of extra legal steps than getting other debts discharged. And, because you sometimes can’t get your student loans discharged even in bankruptcy, it should only ever be your very last resort.

You need to remember that declaring bankruptcy can have long-lasting effects on other financial opportunities in your life, and it can prevent you from borrowing money in the future.

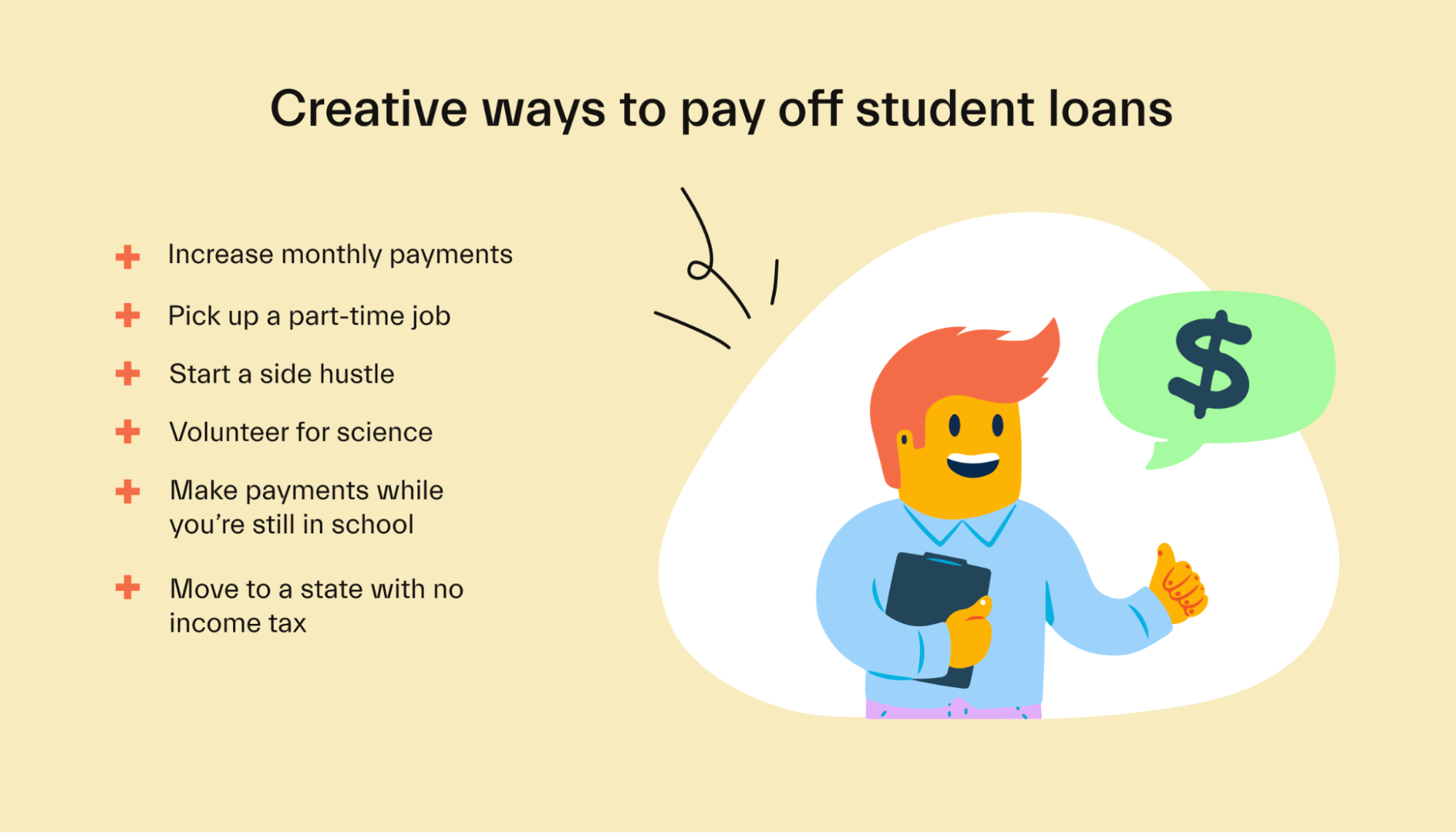

6 creative ways to pay off student loans with extra income

We’ve covered some of the most common ways to pay off student loans on a low income. But there are some creative alternatives worth exploring, too. To help inspire you, we’ll walk you through a few options.

1. Increase monthly payments

This might sound crazy at first but bear with us. Increasing your monthly payments means that you’ll be paying less interest. This means you’ll end up paying less money long-term.

Loan servicers may apply your extra amount to next month's bill by default. Be sure to ask them to apply overpayments to your current balance and keep next month's payment as planned.

You can make additional payments at any point during the month or make a lump sum payment.

2. Pick up a part-time job

Taking up a part-time job like bartending would allow you to earn a decent amount of money in tips after you’ve finished your day job.

This will help you build up a bit more wealth to put towards your loan payments.

3. Start a side hustle

Side hustles are a great way to make extra money.

You could sell clothes, rent out your spare room or parking spot, or use your skills to freelance or consult on the side. Then you can put all that extra money towards your loans.

4. Volunteer for science

You’ve probably seen this in plenty of TV sitcoms—but taking part in research studies is actually an easy way to earn extra cash.

You can get paid hundreds (or even thousands) of dollars to participate in medical research, sell blood plasma, or donate sperm or eggs. It might not be the most conventional way to pay off student loans, but it’s an option.

5. Make payments while you’re still in school

Another way to get a head start on clearing your loans is to start making payments while you’re still in college.

This isn’t mandatory for a lot of student loans—and for some, it won’t be practical. But if you have a good part-time job and some disposable income, making an early student loan payment now could help you in the future.

6. Move to a state with no income tax

Not all states tax equally. There are 9 states in the US that don’t have an income tax. Instead, they tend to make up for tax shortfalls with a higher sales tax.

Translation: if you’re a low earner, moving to a state with no income tax might not be worth it. But if you’re a high earner, you can end up saving a lot! That savings can then be applied to your outstanding debts instead.

Conclusion

No two borrowers are 100% alike, and so the best way to pay off your student loans might be different for you than others.

But it’s important to understand that no matter how much you might be struggling to repay your student debt, there are options out there.

From student loan refinancing and repayment schemes to debt forgiveness and side hustles, there are many opportunities available. You just need to do your research and don’t be afraid to ask for professional help.

Want to learn more about how to pay back your student loans? Check out our guide on what to do when you can’t pay off student loans and visit our learning hub to find out more.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you