Student loans •

June 20, 2022

What are the pros and cons of student loans?

The responsible use of student loans can help you cover the gap between the cost of tuition and free financial aid.

In 2022, the average total cost of college for a first-time, full-time undergraduate student is $35,331 per year.

But don’t let the high sticker price scare you away from getting educated.

There’s plenty of financial aid available out there. Over 83% of college students received some form of financial aid to help make ends meet in 2021.

Some of that financial aid is free, and some of it you have to pay back (student loans). Taking free money is always a good idea. But before accepting a student loan, you need to figure out if borrowing makes financial sense for you.

In this article, we’ll break down what student loans are, their pros and cons, and how to determine if a student loan is right for you.

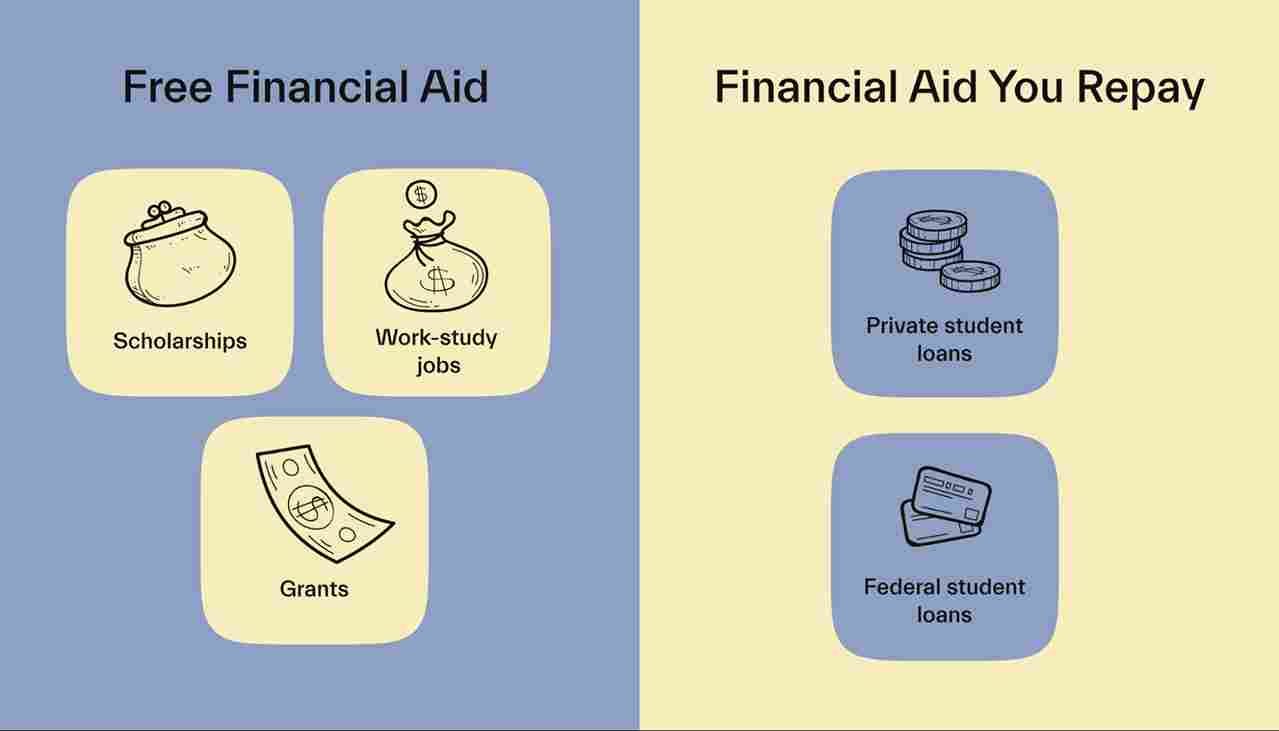

What is financial aid?

Financial aid is money to help you cover the costs of college through the federal or state government, schools, private businesses, or other organizations. Examples of financial aid include grants, scholarships, work-study programs, and federal student loans.

Some financial aid is free—you never have to pay it back. For example, the Federal Pell Grant is free financial aid of up to $6,496 (in 2022) based on your financial need. You don’t have to repay a Federal Pell Grant.

With other types of financial aid, you need to eventually repay it. For example, a Stafford loan is a type of federal student loan that you need to pay back to the Department of Education.

What are the types of free financial aid?

The three main types of free financial aid are scholarships, grants, and work-study programs.

Scholarships

Scholarships are merit-based awards based on your academic performance, extracurricular achievements, or association with specific organizations.

The most well-known scholarship based on academic performance is the National Merit Scholarship, which rewards high scorers of the Preliminary Scholastic Aptitude Test (SAT)/National Merit Scholarship Qualifying Test (PSAT/NMSQT).

Other scholarships are available to students displaying exceptional talent (e.g., artistic talent, athletic ability) or involvement in organizations (e.g., community service, plans to work for a company or within an industry).

Other scholarships are available to students for a wide variety of reasons, including family background, race, or ethnicity.

Grants

A grant is free money for students with demonstrated financial hardships. Grants are need-based financial aid.

The federal government is the main source of grants, budgeting $31.7 billion in federal grants in 2021. Some examples of federal grants are the Federal Supplemental Education Opportunity Grant (available to students with an extreme financial burden), and the Iraq and Afghanistan Service Grant (available to children of military service members who died in the Iraq or Afghanistan wars).

State governments, private organizations, and schools may offer grants as well.

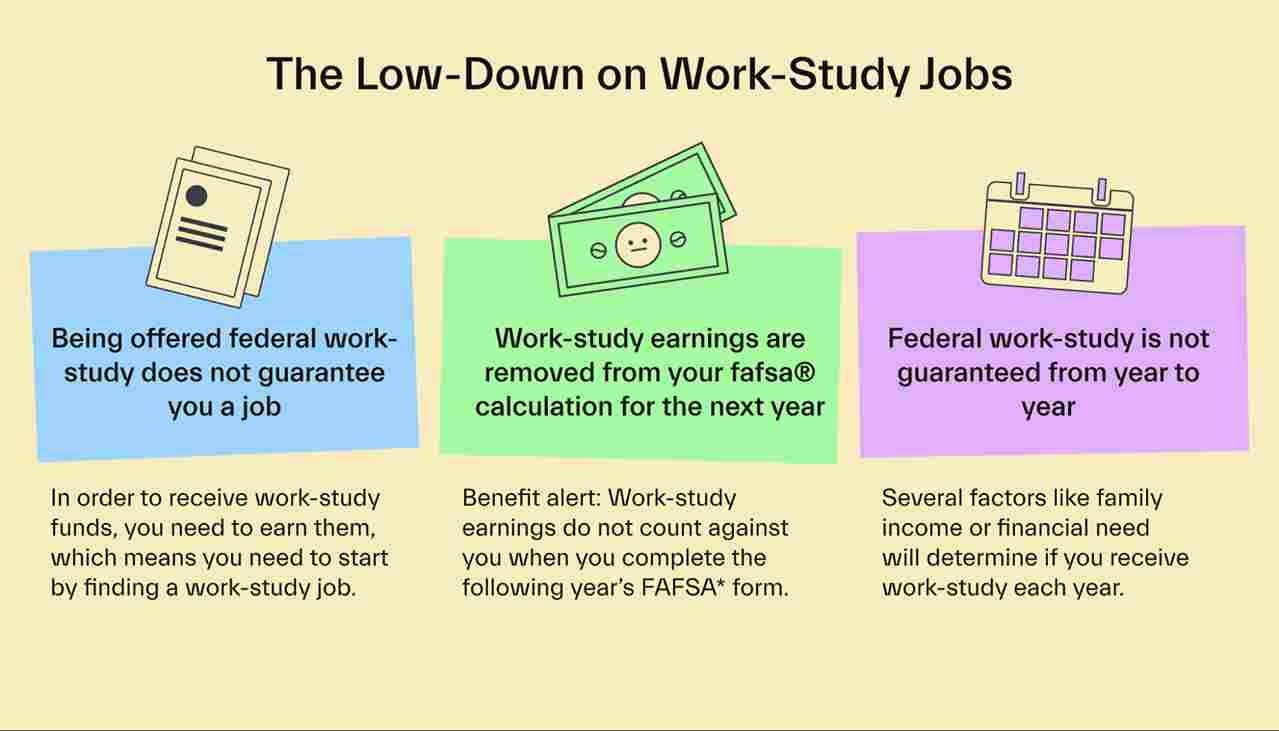

Work-study programs

A work-study program is financial aid that you need to earn by performing an eligible job. Undergraduate and graduate students need to demonstrate financial need to apply for work-study programs.

The application for a work-study program is competitive. In 2021, only 18% of students received such federal financial aid. In addition to the government, local nonprofit organizations and universities employ students through work-study jobs.

What is financial aid that I need to repay?

Typically, student loans are the only type of financial aid that you have to pay back even if you finish your studies without issue. The need for repayment is the main reason you should first maximize your free financial aid before considering student loans.

You can seek to borrow from the federal government (federal student loans) or from private lenders (private student loans).

Federal education loans

The federal government offers federal education loans through the Department of Education. In 2021, the average federal education loan was $8,825 per year.

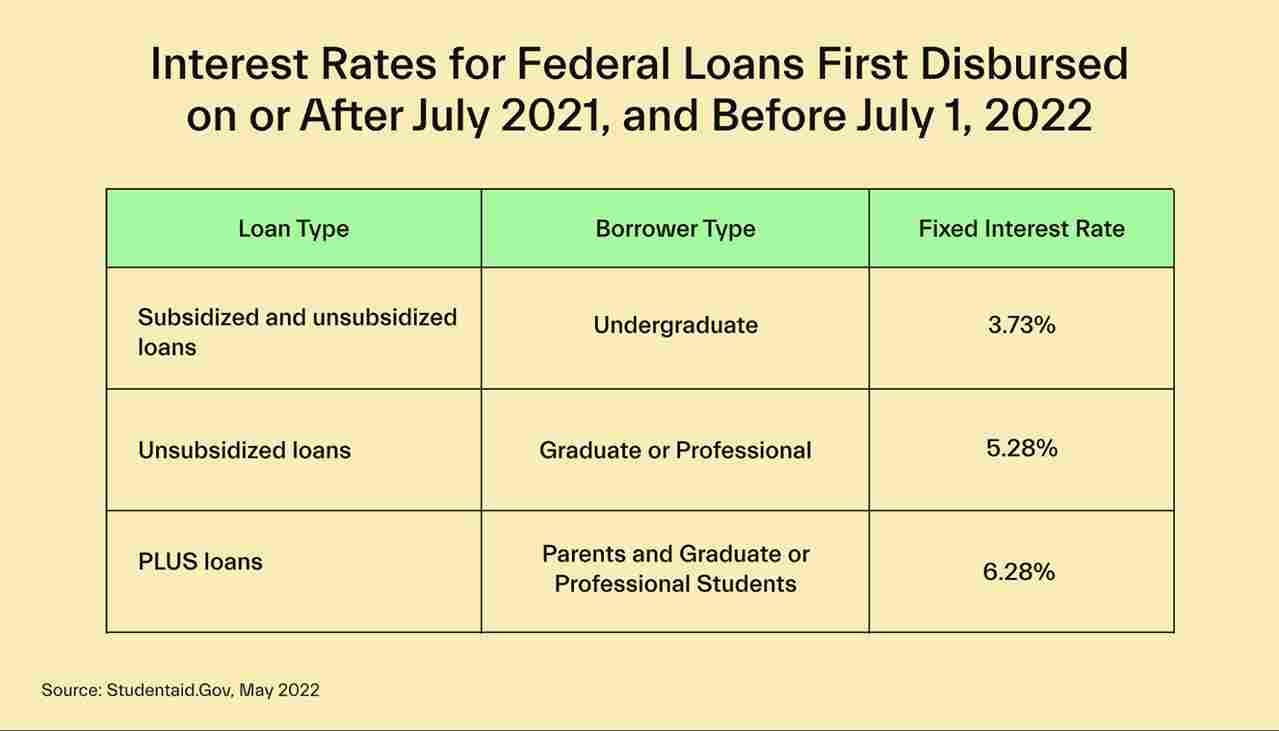

There are four main types of federal loans:

Subsidized loans: The federal government pays for the interest while the undergraduate student attends school. These federal student loan interest payments prevent it from growing exponentially while you are in school.

Unsubsidized loans: This type of loan is available to undergraduate and graduate students. The interest of an unsubsidized loan starts accumulating from day one of the loan.

PLUS loans: An undergraduate or graduate student with a good credit history can use their creditworthiness to apply for a PLUS loan. Also, a parent or guardian may take out a PLUS loan to pay for college degree expenses.

Consolidation loans: After graduation, you can combine all of your federal student loan debt into a single consolidation loan.

Private education loans

In addition to the federal government, other organizations provide loans (private education loans). States, universities, and financial institutions offer private debt to student borrowers.

Private education loans aren’t as common as federal loans. In 2021, 13% of students chose private debt.

How are federal loans and private student loans different?

Federal and private student loans have several key differences:

Interest rate: Typically, federal student loan rates are lower than those of private ones. Federal loan interest rates are set for the life of the loan, while private loan rates may or may not change (variable interest rates).

Loan subsidy: Subsidized federal loans cover your interest payments while you attend school. Most private loans aren’t subsidized.

Start of repayment: All private loans require you to start paying the loan right away. Unless you drop out of college or attend less than half-time, you won’t need to repay a federal loan before graduation.

Loan consolidation: Consolidation loans are an option with federal student loans. A private lender isn’t required to provide a consolidated loan option.

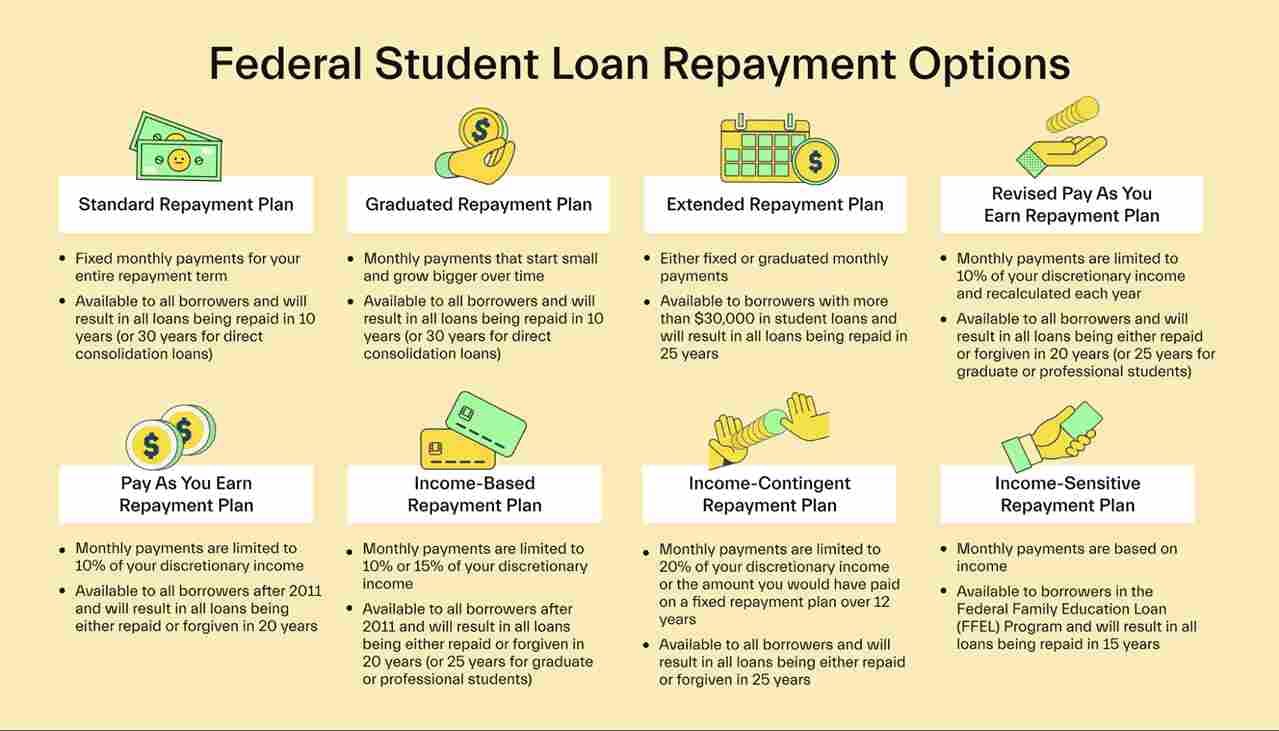

Repayment options: Federal loans provide more flexible repayment arrangements than private loans. Some options include a 6-month repayment grace period and a series of income-driven repayment plans.

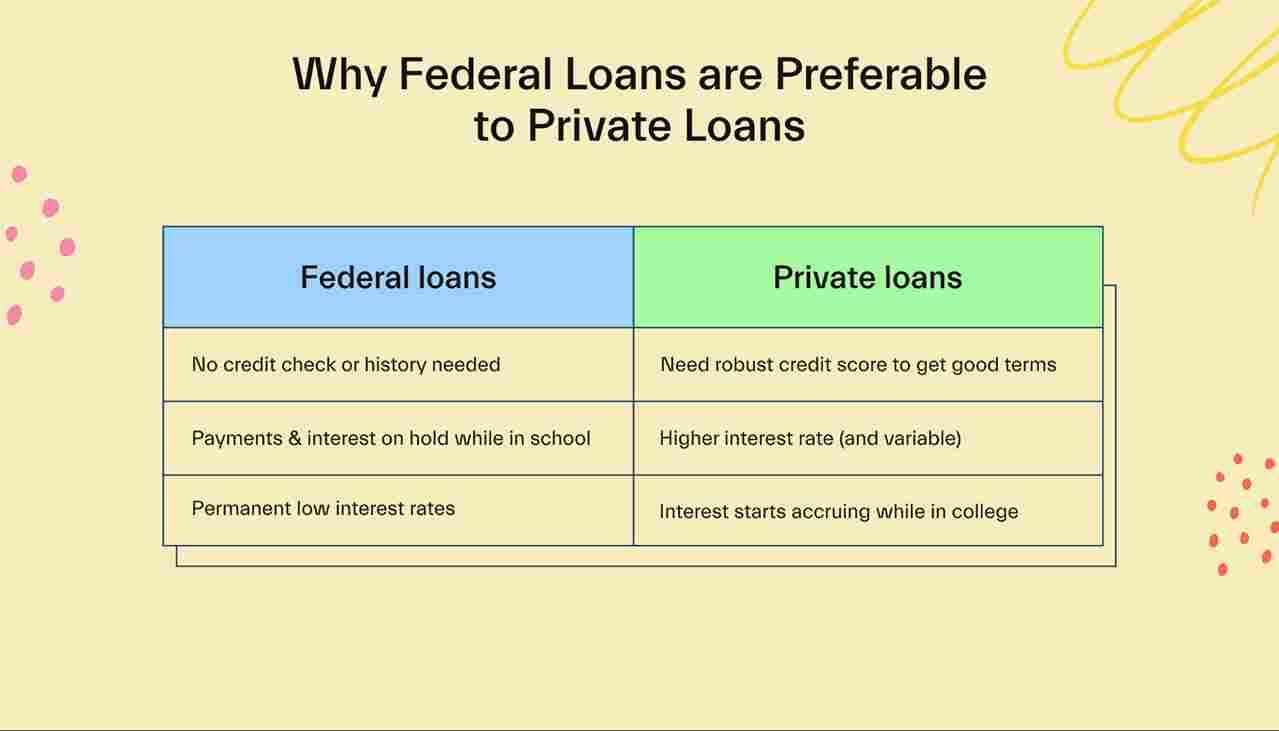

Why are federal loans preferable to private loans?

All things equal, you should exhaust all free financial aid before you consider borrowing. If you do need to take out a student loan, here’s why federal loans are preferable to private ones.

No credit check or credit history needed

With most federal student options, you won’t need to have an existing credit history. Only a few federal options, such as a PLUS loan, consider your credit history when applying.

A federal loan is typically more friendly to first-time student borrowers with little to no credit history.

Payments aren’t due until after graduation

Yes, a federal loan provides you with a grace period of six months after graduation before repayment.

You may also ask to postpone the start of repayment if you’re going through financial hardships.

The government covers interest payments until graduation

One of the major federal benefits is that the government covers interest payments on its subsidized loans until graduation.

Unlike subsidized federal loans, all private loans start charging you interest from day one.

Fixed interest rates and often lower than that of private loans

Currently, the Department of Education has set an interest rate on its loans at 0%. This temporary relief measure is set to expire on August 31, 2022.

Still, the latest schedule of interest rates before the COVID pandemic shows that federal loans have lower interest rates than those of private loans. And federal loan rates aren’t variable rates.

Income-driven repayment plans & loan forgiveness

Federal student loans also offer the opportunity to participate in income-driven repayment plans, and in certain cases, you can even have your remaining federal student loans “forgiven” through special programs.

What are the pros of student loans?

Here are some of the pros of taking on student debt.

Higher earning potential

There’s no way around it: college grads tend to earn more (significantly more) than high school grads.

If a student loan is the only way that allows you to pursue and complete a college education, then it may be a worthwhile investment.

Payment isn’t due until after graduation

Subsidized federal loans allow you to defer payment for up to 6 months after graduation.

If you can’t land a job or suffer financial hardships, you may be able to push back your repayment start date even longer.

Student loan interest deduction

When you take out a student loan, you or your parents may claim a college tax credit or deduction on a tax return.

Some of the available tax breaks include the American Opportunity Tax Credit, the Lifetime Learning Credit, and the Student Loan Interest Deduction.

Credit history

For many students, a student loan is their very first form of credit.

When properly managed, student loans can help you build up a credit history. Your credit score is based on your credit history, and you’ll need one to apply for a car loan, credit card, or mortgage.

Loan forgiveness

Some professions (e.g., nursing, teaching) and industries (e.g., public government) may make you eligible for student loan forgiveness.

Repayment options

Federal student loans offer many repayment options.

Based on your unique financial situation, you may be eligible for making repayments based on your income, applying for a delay on the start of payments, or securing a discharge or forgiveness of your loan.

What are the cons of student loans?

Now, let’s review the disadvantages of having student debt.

Potential delay of other financial plans

In 2022, the average federal loan debt balance for American students stands at $37,104.

While a college degree may increase your earning potential, a hefty school loan debt may hinder your other financial plans.

If you have to put away several hundred dollars in monthly payments, you may have a hard time saving for a home down payment or building a nest egg.

Sign a legal document

Taking on student debt is a serious matter.

To accept a student loan, you have to sign a FAFSA master promissory note (FAFSA MPN).

A FAFSA MPN is a legal document in which you promise to repay your entire loan, all of its applicable interest, and any fees to the US Department of Education.

Additionally, you may have to sign more than one MPN. Your lender may require you to sign a new MPN every year or to take on additional debt.

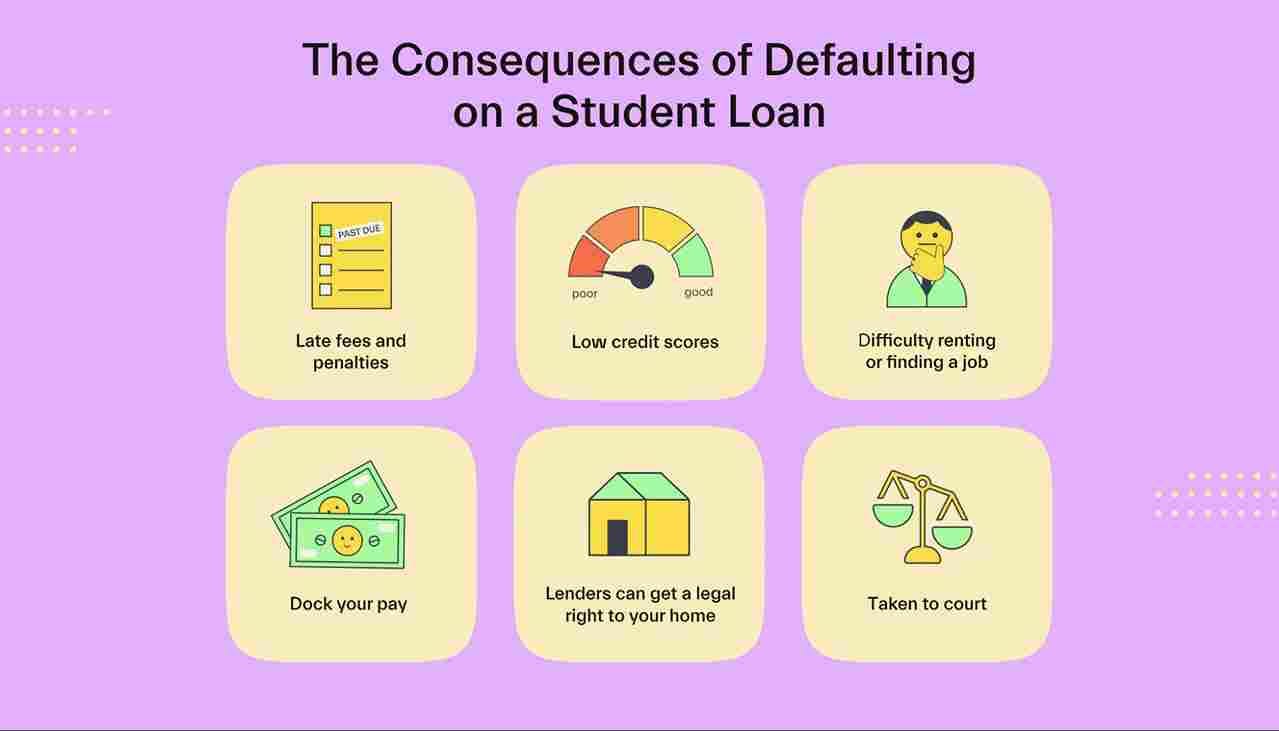

Fees and penalties

Just like responsibly managing your student debt can build up your credit, irresponsibly handling debt can wreck it. If you were to completely default on your debt, your credit history would take a big hit.

Penalties for defaulting on student debt include extra fees, added interest, and wage garnishment. Here’s an overview of what happens when you don’t pay student loans at all:

The good news is that you do have options when you can’t afford your student loan payments. Your lender is often able to help you get back on track with payments. The first step is always to reach out to your lender right away.

What are some criteria to decide if I should take out student loans?

Let’s break down some guidelines for determining if you should take on student debt.

You’ve exhausted all grants and scholarship options

There is free money out there for the taking, but it's estimated that every year about $2 billion in grants go unclaimed.

Make sure to fill out the FAFSA because it allows you to apply for about $120 billion in financial aid every year. Also explore private scholarship and grant options—Mos gives you easy access to the largest scholarship pool in the US.

Can you work sustainably alongside your studies?

Seek out jobs that match your schedule and allow you to cover some everyday expenses, even if you won’t earn enough to fund your studies.

That includes options like:

Work-study programs: The average undergraduate student earned $1,794 through work-study programs per year in 2021.

Job tuition reimbursement: Some employers, such as Bank of America, Starbucks, UPS, and Walmart, reimburse eligible college expenses.

On-campus work: From participating in studies to working in the library, you have many options to earn money on campus.

Can you be flexible with your school plans?

Choosing between in-state and out-of-state tuition can make a big difference in your school budget. Choosing a school in your state may allow you to avoid taking on school debt.

Also, you could consider first moving to the state of your target school, gaining residence, and only then starting attending.

Another option would be to first complete credits at a community college and then transfer to a more expensive school later in your studies.

Make sure you maximize free financial aid first

While you could borrow up to $5,500 in federal loans as a dependent undergraduate in your first year, it doesn’t mean you should.

Student loans are often part of a financial award package. Look for ways that you can increase the amount of free financial aid so that you minimize your loan amount. Remember that you can appeal a financial aid award letter.

Conclusion

Student loans aren’t always the right path to paying for college.

Despite the rising cost of college, it’s possible to complete a debt-free degree. Remember that over 83% of college students received some form of financial aid to help make ends meet in 2021.

After exhausting all free financial aid options, you may have to take out a student loan. The key is to keep a manageable debt load and stick with subsidized federal loans as much as possible.

Sign up for Mos to make sure that you’re not leaving money on the table and maximize your free financial aid from federal and private sources.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you