Student loans •

How to cancel student loan debt

Got a lot of student loans? In certain situations, you can get your loans erased. Learn how to cancel student loan debt and reduce your debt burden.

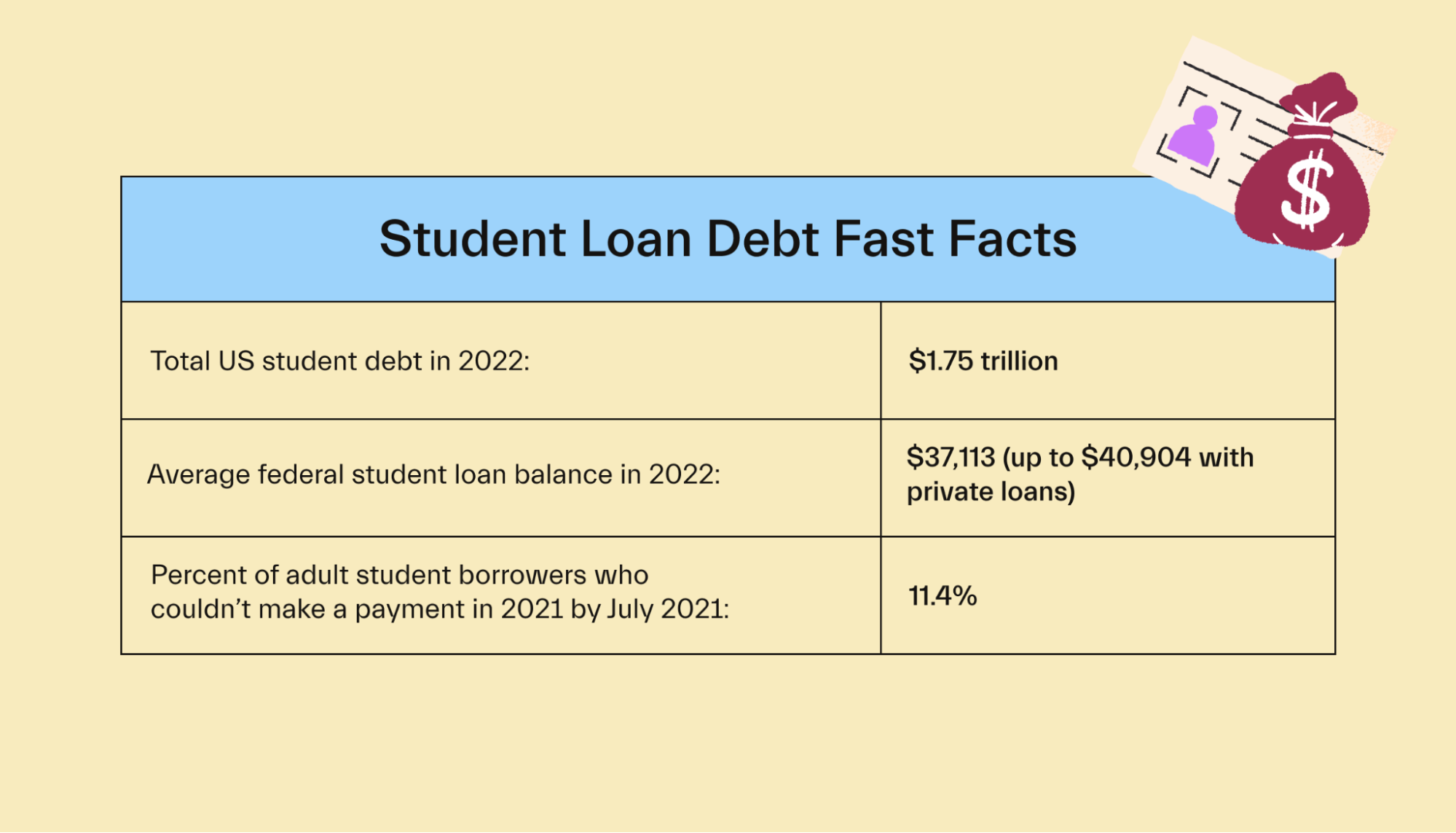

According to the Education Data Initiative, student loan debt in the US sits at almost $1.75 trillion in 2022! If you think that sounds like a lot, that’s because it is. Student debt represented 7.6% of the entire US GDP in 2021.

So student loan debt is clearly a problem. But luckily, there are several programs that can help you cancel student loan debt—your own, that is.

That means your loans could be completely erased if you qualify for any of these programs—sounds like a good deal, right?

In this article, we’ll explain how student debt cancellation works and cover several payment plans, forgiveness programs, and other methods that offer it so you can see if you qualify.

What does student loan debt cancelation actually mean?

If your student loan debt gets canceled, you no longer have to pay it back.

When it comes to cancellation, there are two types: forgiveness and discharge. Forgiveness erases your student loans after making on-time payments for long enough if you work within a specific sector.

Discharge erases your loans under other circumstances, such as if you become disabled or a school defrauds you.

Debt cancellation can be a big help—after all, the average federal student loan balance sits around $37,000 per borrower in 2022.

Plus, by July 2021, about 11.4% of borrowers with student debt claimed they couldn’t make at least 1 of their payments that year to date.

Usually, only federal loans can get canceled. Most private lenders don’t let you cancel loans without serious circumstances, like death, disability, or another rare occasion dictated by the government.

Speaking of that, the Biden administration made student loan cancellation a big piece of their platform. However, President Biden’s recently proposed 2023 budget doesn’t mention student loan forgiveness or payment pauses.

Student debt cancellation and taxes

When you borrow money to pay for school, you eventually have to pay it back. If that debt’s canceled, it’s basically like you got paid the money in the first place.

Therefore, the IRS may consider a canceled student loan to be income. However, if your student debt is canceled as part of a federal debt forgiveness program, in most cases, canceled student loans aren’t taxed—you just need to report them in your tax filings. Plus, the majority of student loans canceled between 2021 and 2025 are exempt from taxation. Also, note that these rules could change if the government takes more action to provide student borrowers with financial relief.

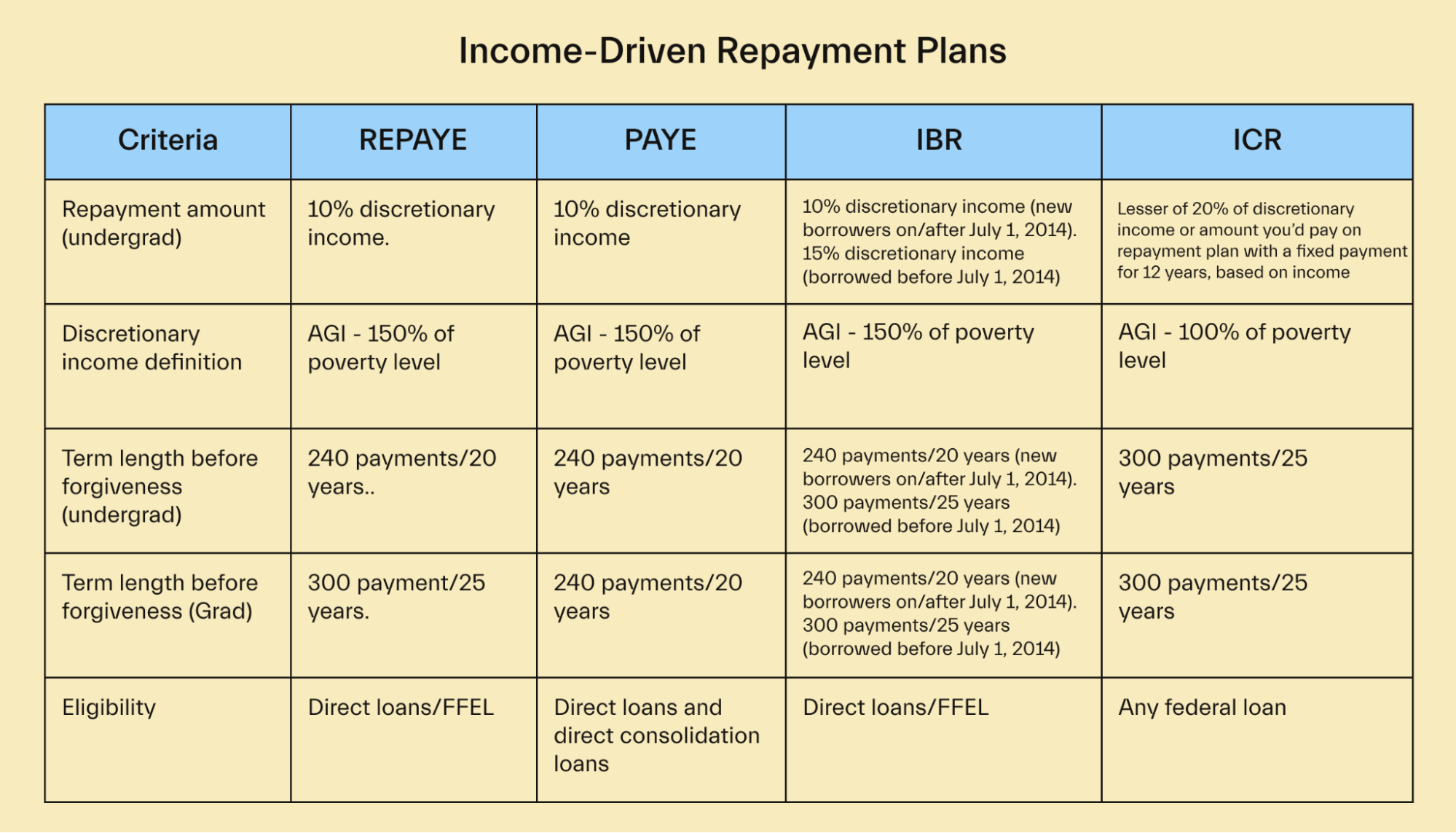

How to get student debt canceled: Income-driven repayment programs

Income-driven repayment plans use your income and family size to set your monthly student loan payment at an amount you can afford.

Each plan has a few rules to be eligible. They each calculate your payment based on your discretionary income, which is defined differently depending on the plan. Your payments can change each year as you recertify your income.

Regardless, they’ll often be lower than what they’d be under a Standard Repayment Plan. As a result, you might not pay off your entire balance during your repayment period.

That’s ok because they all offer loan forgiveness after making monthly payments on time for long enough.

Here are the details for each plan:

Revised Pay As You Earn

Anyone with eligible federal loans as defined by the Department of Education (ED) can qualify for the Revised Pay As You Earn (REPAYE) program.

Under REPAYE, your loan payment becomes 10% of your discretionary income, which is defined as your adjusted gross income minus 150% of your area’s poverty level.

If all your loans were used for undergrad education, you could qualify for loan forgiveness after 20 years—which involves making 240 successful monthly payments.

That number jumps up to 25 years, or 300 successful payments, if any loans under your REPAYE plan were used for professional or graduate studies.

Pay As You Earn

To qualify for a Pay As You Earn (PAYE) plan, you must be considered a new borrower as defined by the ED.

Under PAYE, your loan payment becomes 10% of your discretionary income, which is defined as your adjusted gross income minus 150% of your state’s poverty guidelines. That said, your payment can never be more than the 10-year Standard Repayment Plan amount.

After 20 years or 240 payments, the remainder of your eligible loans can qualify for forgiveness.

Income-Based Repayment

Anyone with eligible federal loans as defined by the ED can qualify for an Income-Based Repayment (IBR) plan. However, your payment varies depending on when you borrowed your loans.

For new borrowers on or after July 1, 2014: Your loan payment becomes 10% of your discretionary income, but never more than the 10-year Standard Repayment Plan amount.

For borrowers that were not new borrowers on or after July 1, 2014: Your loan payment becomes 15% of your discretionary income, but never more than the 10-year Standard Repayment Plan amount.

Once again, discretionary income is defined as your adjusted gross income minus 150% of your state’s poverty guidelines (based on your family size).

Your repayment period length before forgiveness depends on the same thing:

For new borrowers on or after July 1, 2014: Your repayment period before forgiveness is 20 years or 240 periods if you were a new borrower on or after July 1, 2014

For borrowers that were not new borrowers on or after July 1, 2014: Your repayment period before forgiveness is 25 years or 300 payments.

Income-Contingent Repayment

Income-Contingent Repayment (ICR) plans are available to anyone with eligible federal loans as defined by the ED.

Under an ICR plan, your loan payment becomes the lesser of:

20% of your discretionary income

Your expected payment on a repayment plan with a fixed payment over 12 years, adjusted according to your income

In this case, however, discretionary income is defined as your adjusted gross income minus 100% of your state’s poverty guidelines (instead of 150% like in the other plans).

As for forgiveness, you must make payments for 25 years, equal to 300 payments, before having your loans forgiven.

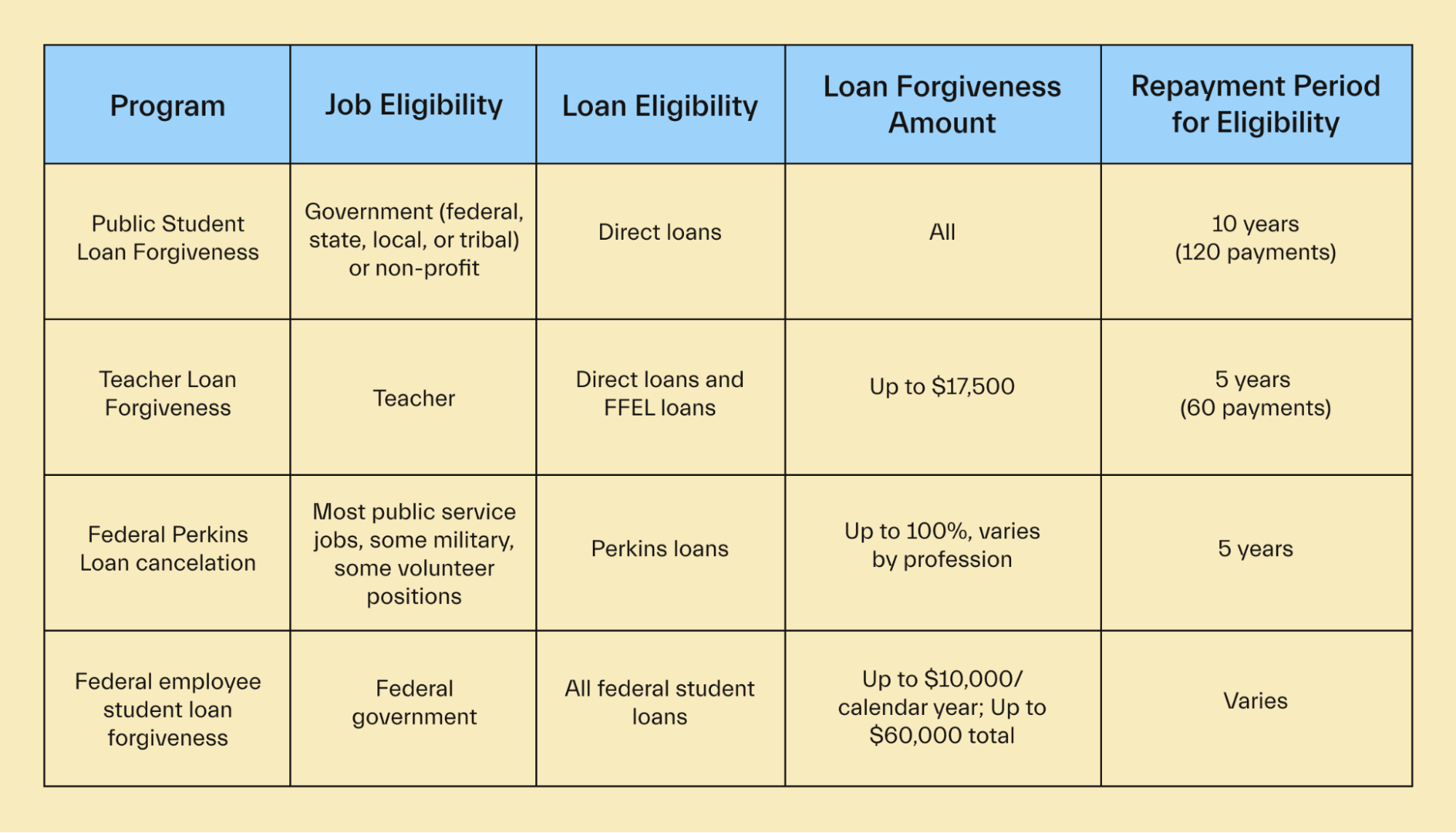

Loan forgiveness programs that could cancel your student debt

Income-based repayment plans are the main way for most people to get their federal student loans canceled.

However, there are a few special loan forgiveness programs for people that work in certain jobs or industries. Most require you to be on an income-based plan, but loan forgiveness comes much sooner.

Check out these loan forgiveness programs to see if you qualify:

Public Service Loan Forgiveness

The Public Service Loan Forgiveness is one of the most well-known programs in the country. It’s designed for anyone who works for federal, city, state, or tribal governments. This includes government employees, teachers, and public safety officials like police officers and firefighters, to name a few.

Not-for-profit employees may also qualify for PSLF.

If you’re in an eligible job, you have to meet the following:

Have direct federal student loans or consolidate other loans into direct federal loans

Work full-time

Make on-time payments for 10 years (120 payments)

Repay loans on a qualifying income-driven repayment plan—although this is waived until October 31, 2022.

After those 10 years are up, you can apply to have your remaining eligible federal loan balance wiped clean by filling out the free online application.

Teacher Loan Forgiveness

PSLF can help you erase all your loans, but it takes 10 years to qualify for.

Fortunately, if you’re a teacher, you could get some of your loans erased sooner through the Teacher Loan Forgiveness program.

To qualify, you generally have to teach full time for 5 complete consecutive academic years in a low-income school or educational service agency. Direct and FFEL loans are eligible.

If you qualify, this program could forgive up to $17,500 in Direct or FFEL loans after your 5th year.

There are plenty of nuances regarding what is a “low-income” school or educational agency and how to count years where you spend only part of the year teaching. Federal Student Aid goes over the requirements in more detail here to clear those things up.

Federal Perkins Loan cancelation

The Perkins loan program was phased out in 2017, but many borrowers still carry these loans.

Fortunately, many public service employees can have these erased under Federal Perkins loan cancellation.

The ED’s Federal Student Aid office provides a lot of detail on how teachers can have their Perkins loans canceled. However, exact requirements can vary by profession.

Per Federal Student Aid, you can contact the school that made the Perkins loan to you or that school’s loan servicer to get the proper forms and directions for applying for forgiveness.

Federal employee student loan forgiveness

Work for the federal government but don’t qualify for PSLF or Perkins cancellation?

Don’t worry—according to the US Office of Personnel Management, federal agencies can offer federal student loan repayment as a hiring incentive to fill their positions.

It’s not total forgiveness, but the agency or department you work for could help you pay for part or all of your loans, including Perkins loans if you’re in good standing at work.

Per the US OPM, your agency can pay you up to $10,000 per calendar year in student loan repayment assistance. The total repayment allowed caps at $60,000.

Of course, the total amount will vary depending on which agency you work for. Contact your HR department to get the details.

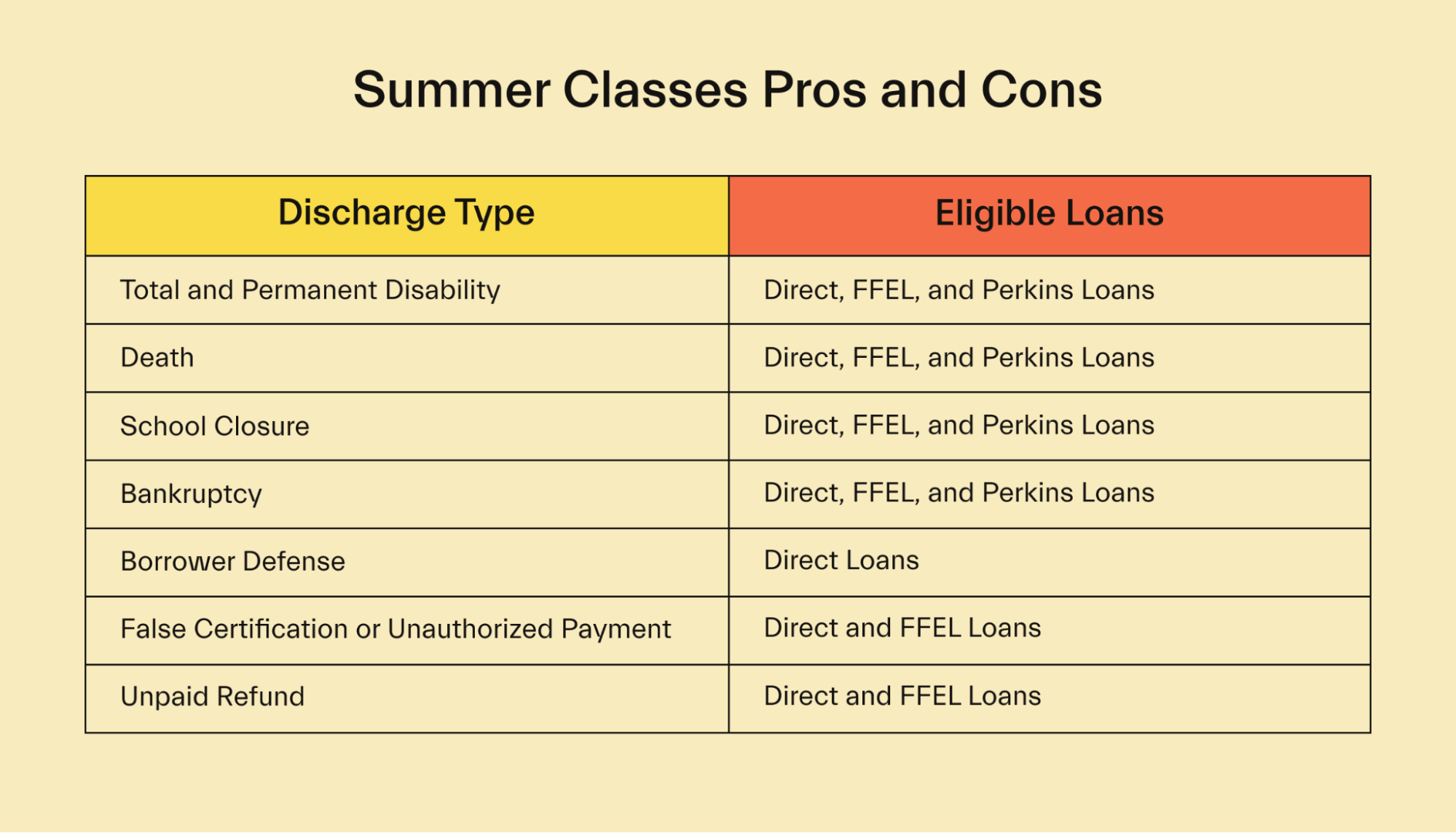

Student loan discharge

Discharge is slightly different from forgiveness—it erases loans if you can’t pay them back, you’re a victim of fraud, and you have other circumstances that are more “out of your control.”

There’s not necessarily a fixed amount of time that you have to pay back your loans before qualifying.

Many of these discharges used to count as income, but the American Rescue Plan—passed to assist the country during the pandemic—has waived any taxes associated with discharge.

Regardless, here are the ways you could have your loans discharged.

Total and permanent disability discharge

If you become totally and permanently disabled, as defined by Federal Student Aid, you can get your loans discharged.

To prove a disability for loan discharge purposes, you’ll need documentation from the Department of Veterans Affairs, the Social Security Administration, or a doctor.

Death discharge

If you die with outstanding federal loans, those loans will be discharged. PLUS loans are discharged if either you or the borrower—aka your parent—die while the loan is outstanding.

This means your loans won’t pass onto anyone else.

School closure discharge

Sometimes, schools close down for good. If your school closes while you attend or shortly after withdrawing, the government may discharge your federal student loans.

Make sure you meet the requirements before applying for discharge.

Bankruptcy discharge

Bankruptcy discharge is rare, but you may qualify if the following apply to you:

You would not be able to maintain a minimal standard of living if you’re forced to repay the loan

There’s evidence this hardship will continue for a significant part of the repayment period

You made good-faith efforts to repay the loan before filing bankruptcy

Even if the court grants you discharge, you may only have some of the loans discharged. In some cases, you may simply get a lower rate or other more favorable terms without any true loan cancellation.

Borrower defense discharge

If your school defrauded you in some way, and you can prove it, you can get your loans discharged.

This is more likely to happen with for-profit schools. ITT Technical Institute is a prominent example, having allegedly defrauded millions of students over several decades before closing. Many former students are having their loans used to attend ITT Tech discharged.

False certification or unauthorized payment discharge

If your school falsely certified your eligibility for loans, that’s not your fault. So you can get your loans discharged.

For instance, you could be an identity theft victim—if someone took out loans in your name, you could get them discharged.

Another example would be the school certifying you as eligible to take on loans when you’re not actually eligible. Again, that’s the school’s fault, so the government will discharge those loans.

Unpaid refund discharge

If you withdraw from your school, but your school doesn’t refund unused loans to the ED or the relevant lender, you could get these loans discharged since you didn’t use them.

Get your loans erased

There are plenty of ways you could qualify for student loan debt cancellation, forgiveness, or discharge. But even if you think you’re eligible, it takes time to apply for these programs and wait for your application to process.

You should keep paying your loans until you get written confirmation your loans will be erased. The last thing you want is to face the consequences of unpaid loans while you’re seeking forgiveness.

If you don’t qualify for any of these programs, or you’re struggling to keep up on loan payments while waiting for approval, we got you. Read our guide on getting out of student loan debt for more tips.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you