Budgeting •

August 17, 2022

Making a budget? Here are some personal budget categories to consider

Taking your college finances into your own hands? Here are some personal budget categories to help you create your budget.

Are you thinking about making a budget? Congratulations! You’re ahead of many of your peers.

However, you may quickly get overwhelmed with the first step—noting all of your expenses and breaking them down into categories that make sense within your budget. Everything needs to be accounted for so you can decide where to cut or rearrange your spending.

Otherwise, you risk making money decisions based on incomplete information… which can lead to overspending and financial stress.

Below, we’ll explain why you should make a budget in college and dive into some of the most vital categories to include in yours.

What is a personal budget?

A personal budget is a plan detailing the money you bring in and how you’re going to spend that money.

Personal budgets are broken down into three broad categories:

Income: This is the money you receive from any sources, such as a paycheck, student loans, scholarships, or a birthday gift.

Expenses: These are all the things you spend money on.

Savings/Investment: Your financial goals, retirement accounts, and other savings or investment accounts.

Having these written down helps you manage money—and we all know how important that is as a broke college student.

It’s also an important life skill, as we’ll get into later.

Now, your income can only come from so many places.

Expenses? There are nearly endless things you can spend your money on. Your budget's not very useful without knowing exactly where your money’s going.

To make a helpful budget, you have to break down your income and expenses into categories and subcategories — paying extra attention to the expenses side.

Why do I need a budget in college?

With exams to study for, club meetings to attend, and a social life to maintain, making a budget can seem like extra work.

However, that work can pay off in spades. Here are some reasons why:

It helps you manage your money better

Writing down your financials in a budget makes money management faster and easier.

You can set fixed amounts, percentages, or ranges for the amount you spend, then simply follow that plan. No guessing at whether you’ve spent too much at any given point.

It also makes you use that money more smartly. You have a written plan holding you accountable. You feel bad if you go overboard in any given area, but you also have a plan you can adjust later if that extra spending is necessary.

It can ease financial stress

Writing things down can be cathartic. Not only will you feel better by getting things down on paper, but you’ll have hard proof that you’re bringing in enough income to handle your expenses.

You’ll also feel more organized and in control just by having a monthly budget plan. As a result, you’ll feel a little less money stress.

Even if your budget is tight, you’ll feel better seeing the numbers in front of you.

You can save for your wants

If you want something, you have to save for it. These wants can be small, like a concert ticket or some new clothes.

Or they can be far larger, like a big vacation or future home.

Whatever it may be, a budget lays out where all your money’s going. This makes it easier to designate a certain amount of money to go towards saving for those wants.

You can also find ways to cut expenses, helping you save even more.

Budgeting is an important life skill

Budgeting isn’t just for college students. It’s a vital life skill. As you gain more responsibilities — like a mortgage and family — you need a budget.

Learning how to budget early in life, before you have a ton of responsibilities, will pay off later when your money management skills are superb (and super necessary).

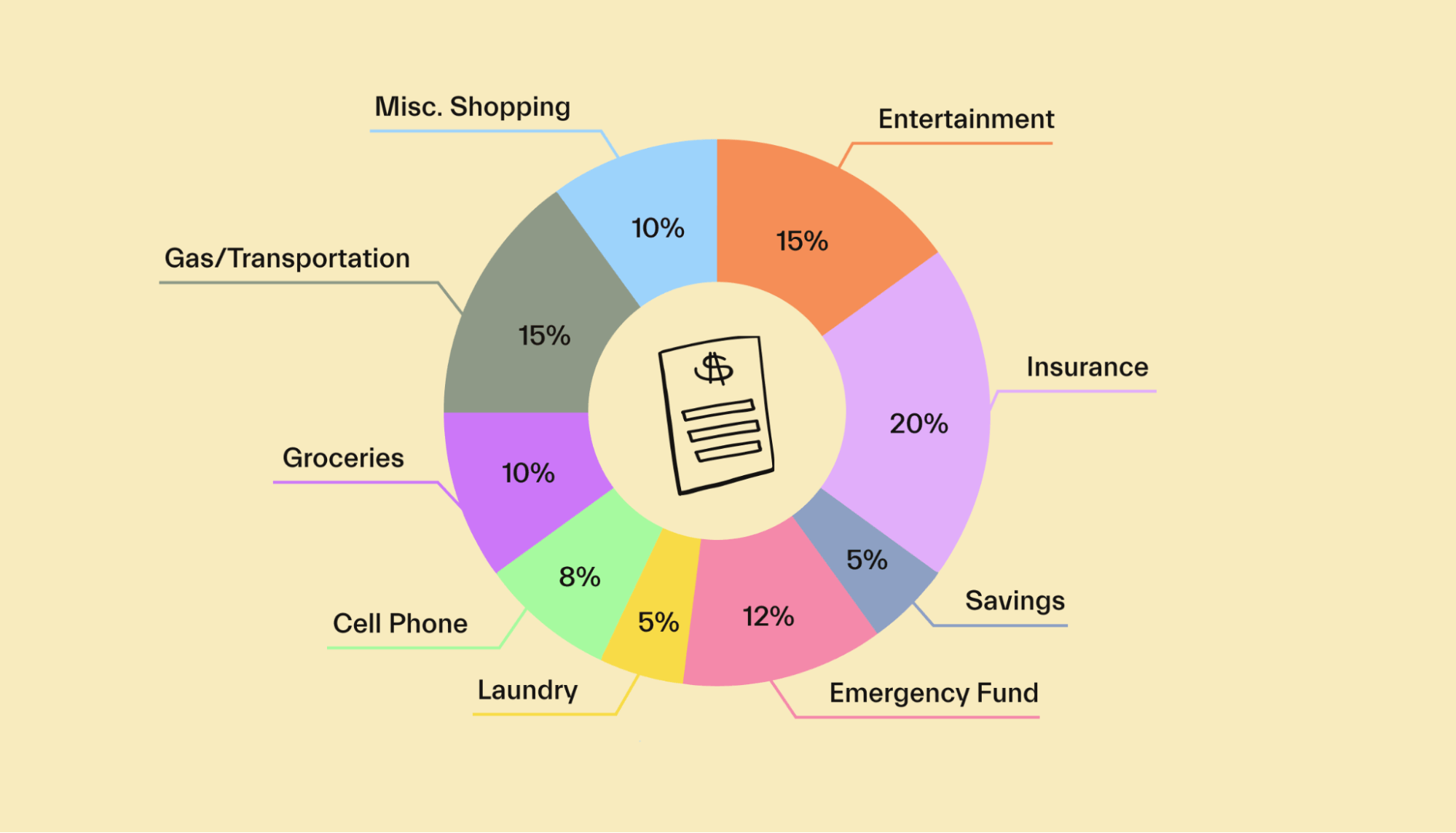

Personal budget categories: The essentials

Before you can list your budget numbers, you need to know which categories and subcategories to include.

Some may belong in multiple categories depending on spending. For example, if you meet up with friends at the bar for drinks, you may place that in “fun” spending. But if you go to that same bar to eat dinner, that may fall under “food.”

Ultimately, these types of expenses are up to you. But here is a list of categories and subcategories to consider.

Income

As mentioned, income is any money you receive aside from refunds or returns. Here are some common income subcategories:

Salary & wages

Self-employed income

Student loans & scholarships

Dividends

Gifts

Interest

Alimony

Child support

Some income, like dividends or alimony, may not apply to you in college.

Depending on how you budget, you might want to include financial aid as well—especially if you use it for more minor expenses, like books.

Housing

Housing is most likely your largest living expense. Debt.org found that public school room and board averages around $8,887/year, and that rises to about $10,089/year at private schools.

Debt.org also found that the average 2-bedroom apartment rent averages $1,178/month.

Of course, there are other expenses involved in housing. Here are some subcategories to include in your budget:

Mortgage/rent

Furnishings

Repairs/maintenance

HOA (Home Owners Association) fees

Property taxes

Again, categories like property taxes and HOA fees may not apply if you aren’t a homeowner.

Utilities

Utilities can vary in cost from month to month, and you may not have to pay for all of them. If you live in an apartment, you’re likely responsible for more utilities than in a dorm.

Per Debt.org, apartment electric bills average $112/month for electric. Other utilities will add to that number if you have to pay for them.

Here are some utilities you may have to pay for:

Electricity

Gas

Water

Trash collection

Internet

Food

Food’s another essential, whether you have a meal plan, go grocery shopping, or some combination of each.

Here are some subcategories to include in your food budget:

Groceries

Fast food

Coffee shops

Restaurants

You can include bars here if you enjoy going out for drinks, but that may also be in a “fun” category. That’s up to you.

Transportation

Some students drive. Others ride the bus. Hipsters, extra broke students, and health nuts bike, walk, or longboard to class.

Regardless, you may have some transportation expenses to pay for. Here are a few subcategories to consider adding:

Car payment

Gas

Car warranty

Repairs

Car registration/DMV fees

Parking fees

Tolls

Public transit

Maintenance/oil changes

Insurance

Even as a student, you may have your own insurance policies. Here are some to include in this category:

Health insurance

Dental insurance

Vision insurance

Homeowners/renters insurance

Car insurance

You may consider adding things like car insurance to transportation, but for many, putting all insurance expenses in their own category makes the budget organization simpler.

Healthcare

Unfortunately, your health insurance may not cover everything. You may need to budget for healthcare expenses, such as the following:

Out-of-pocket costs

Co-pays

Urgent care

Specialty care

Prescriptions

You might include over-the-counter medications here, depending on the medication and what it’s used for, but you could also place it in your groceries subcategory.

Saving/Investing

Yes, it’s possible to save money in college and invest as a college student—even on a tight budget.

Doing so now lets you take advantage of the power of compound interest to get ahead. Plus, you’ll learn valuable lessons about investing when you have less money and responsibilities to worry about.

You might have been saving since you were a teenager and got your first job, or maybe this is your first attempt. Start by breaking down the subcategories of saving, investing, and debts by your personal goals.

Some examples of different savings subcategories by savings goal include:

Emergency savings

Travel savings

Car down payment savings

Some examples of investing subcategories may include:

Retirement

Starting a family

Stock market “play” money

Any debt payments beyond the minimum can also fall under investments. When you pay down debt, you reduce interest charges, which is essentially earning a return.

For debts, split up categories by the debt itself. You may have a subcategory for student loans, credit cards, a car loan, and so on.

Personal budget categories: The fun stuff

Half the point of a budget is freeing yourself from financial stress so you can enjoy your life.

So it only makes sense that you’d budget for some fun times. Nothing wrong with spending money on yourself if you have some leftover, but you don’t want to go overboard.

Here are some categories that typically land on the “wants” side of things (unless your goal is to be a travel writer, fashionista, or music critic):

Recreation

College is a time to get out there, try new things, grow through your hobbies, and have fun doing it all.

So here are a few subcategories you may want to include in this section:

Travel (for vacation)

Concerts

Streaming services and other subscriptions

Hobbies

Sporting events

Of course, feel free to create other subcategories for recreation and fun if you have them.

Personal spending

You deserve to spend money on yourself sometimes. As long as you budget properly for personal spending, you can stay financially responsible while having a solid quality of life.

With that in mind, here are some personal spending subcategories to consider:

Gym membership

Club dues

Shopping

Gifts

Miscellaneous

The miscellaneous category is where you can place any expenses you haven’t accounted for. Perhaps it doesn’t fit well anywhere else, or it's a large one-time expense you don’t want to mix in with your regular spending.

The miscellaneous category can also be a place for you to allocate excess spending from certain categories. This helps you reduce spending elsewhere to stay on budget. Using a budgeting app to track your spending makes it easier to catch when you’ve overspent in a certain category.

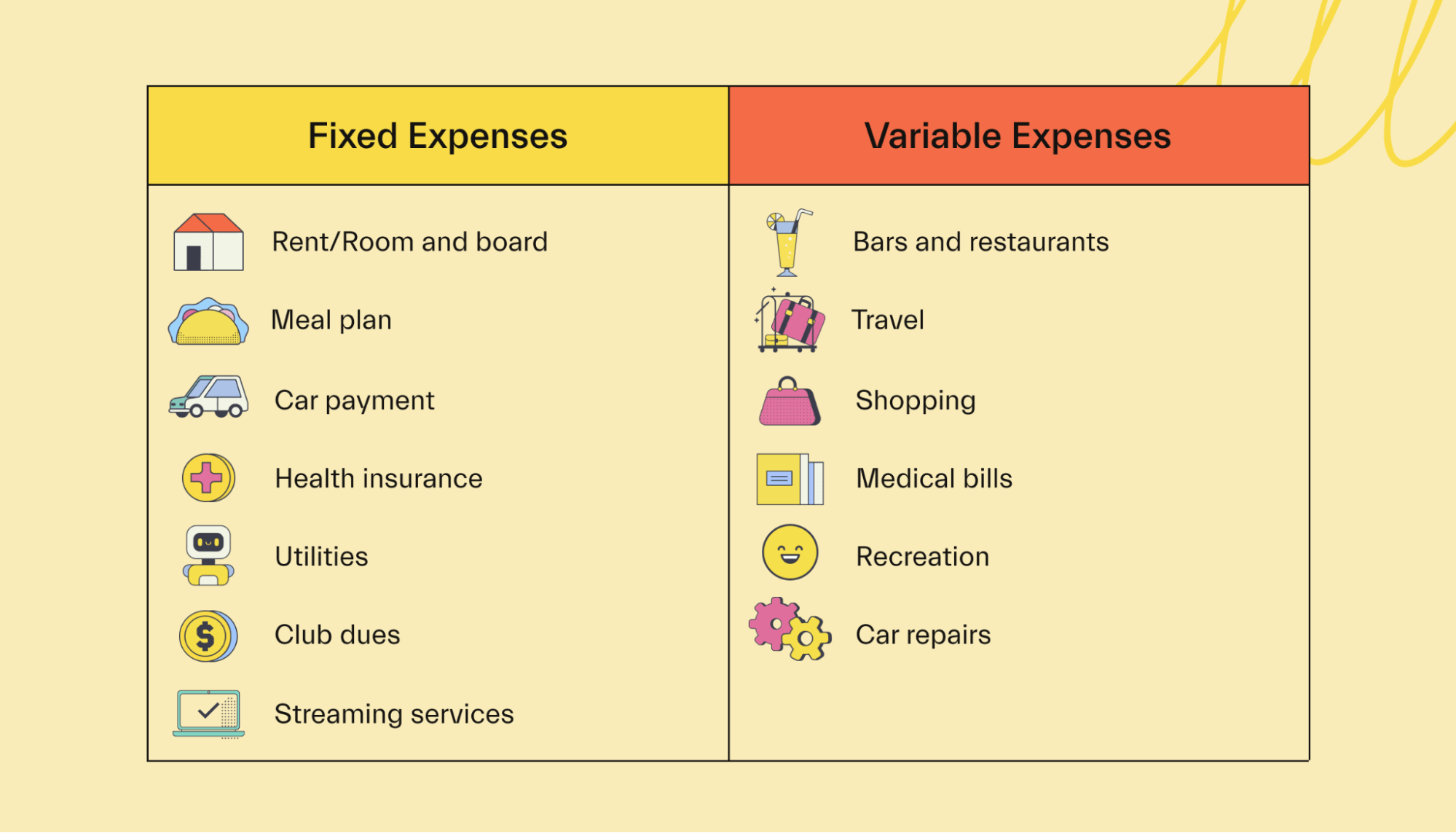

Fixed vs. variable expenses

Now you know some of the categories and subcategories to put in your budget.

But you also need to know the difference between fixed and variable expenses to master personal budgeting:

Fixed expenses

Fixed expenses are expenses that don’t change in amount from month to month. They’re the easiest things to budget for because you know exactly what you’ll pay each month.

That can also make them harder to cut, though, because their very nature doesn’t let you reduce the amount you spend so easily.

For example, you can’t really change your rent without moving or your car payment without getting a new car.

There is some flexibility, though. “Wants,” like your Netflix subscription, are easier to cut because you can change your plan or drop the subscription completely.

Variable expenses

Variable expenses can change from month to month. This makes them slightly harder to budget for, but after a few months, you can get a general range for what you spend on them.

For instance, take your electric bill. If you live in the same place for more than a year, you get a general idea of how much you pay each month throughout each season. You can then plan your monthly budget around that range.

That said, you can cut most variable expenses by using them less.

Back to the electricity example—there are plenty of ways to reduce energy use and slash that bill.

It’s time to make your budget

Everyone’s budget will look different. People have different incomes and priorities, and they’ll spend their money accordingly.

That said, most college students will have many of the above categories somewhere in their budget. These are some of the most common expenses you’ll encounter in college and beyond—don’t forget to include them in your budget if they’re relevant to your circumstances.

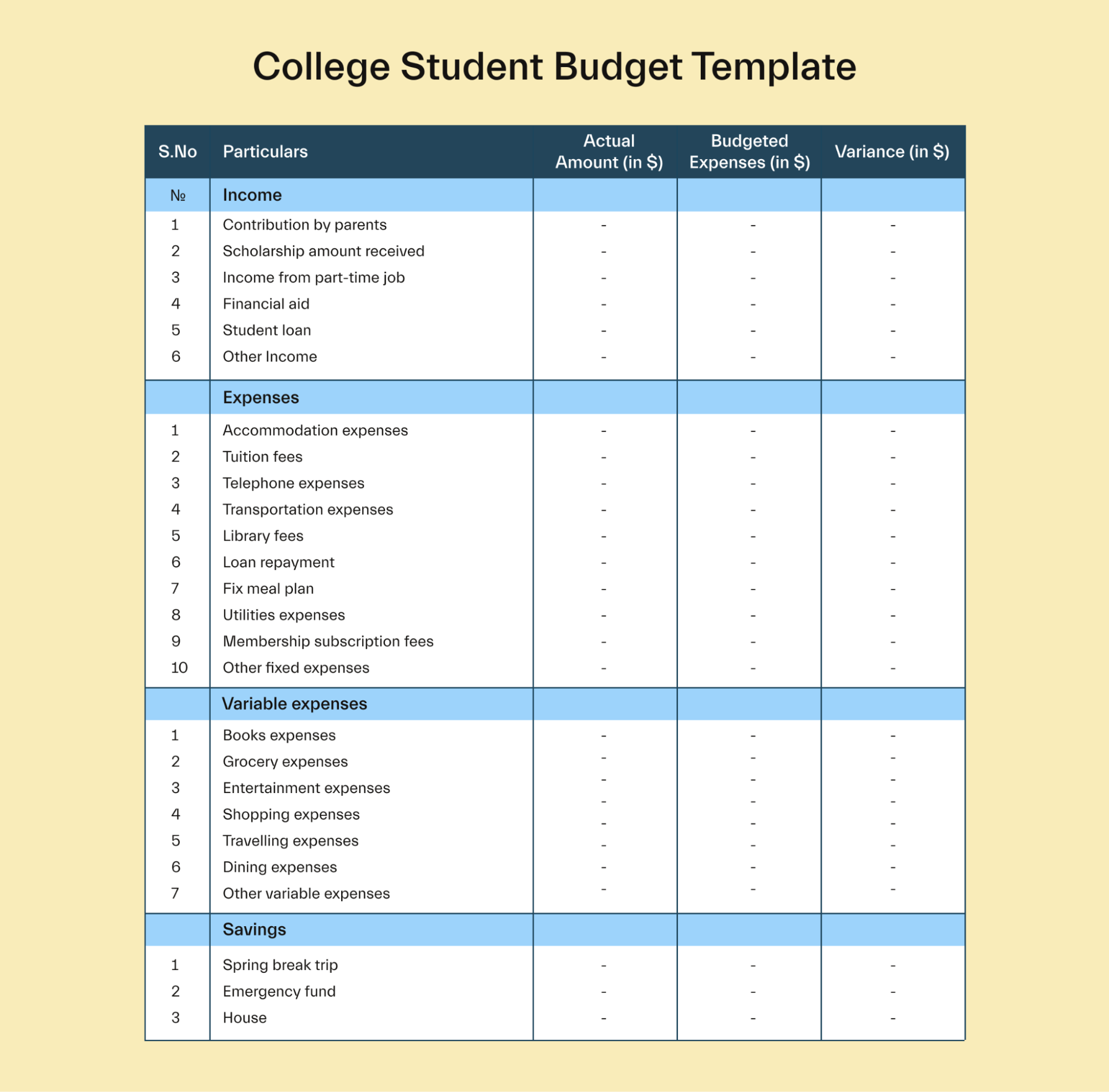

Now that you know what to include in your budget, it’s time to learn how to make that budget. Check out our post on college student budget templates if you need help with that.

Need a hand with the financial aid stuff? Mos gets you an expert’s help with FAFSA, grants, scholarships, and more. Connect with your advisor today.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you