Student loans •

June 20, 2022

Student loan wage garnishment: what it is and how to protect yourself

Learn what student loan wage garnishment is, why it happens, and how you can stop (and prevent) your wages from being garnished.

No one wants to default on their student loans and have a big chunk of their paycheck taken away to cover the debt. But that's exactly what happens when you don't (or can't) make your payments.

If you're worried about student loan wage garnishment and you're not sure what to do next, or Uncle Sam is already "taking his cut" from your pay, and you want him to stop, then you're in the right place.

In this article, we'll talk about what student loan wage garnishment is, how it happens, and how you can stop it. We'll also dish out some tips on how you can avoid it entirely.

What is student loan wage garnishment (and why does it happen?)

Have you ever wondered what happens when you don't pay your student loans?

The good news? You won't go to jail—that’s not how student loans work.

The bad news? You’ll face a series of stressful, long-term consequences—one of which is wage garnishment.

Student loan wage garnishment is when your student loan lender withholds a chunk of your income to pay back your student debt. And it happens because you’ve neglected to pay your loans and defaulted on your debt.

Federal student loans enter default if you fail to make payments for 270 days. Private loans work similarly.

Now, keeping your loan in good standing is the best tactic to avoid defaulting and having your wages garnished. But sometimes life deals you a lousy hand—and that’s understandable.

Just remember that wage garnishment isn’t the end of the world and that there are ways to prevent and stop it once you’ve been served a garnishment notice.

Can private student loan lenders garnish your wage?

Private loan lenders can garnish your wages if you’ve defaulted on your student loans, though the process differs from wage garnishment for federal loans.

We’ll explore the process for both federal and private loan wage garnishment next. For now, the vital thing to remember is that both private and federal lenders can garnish your wages if you miss enough monthly payments.

What happens when student loans garnish your wages?

Here we’ll explore what happens when your student loans are garnished. We’ll discuss federal and private student loans separately, as they each follow a significantly different process.

Federal student loans

After missing 270 days of payments, the US Department of Education (the lender) passes your defaulted loans to their collections office, the Default Resolution Group (DRG).

Once the DRG takes control of your loan, it can start garnishing your wages using its administrative wage garnishment process (AWG).

The AWG is a powerful debt collection process, granting any federal agency the power to garnish up to 15% of any non-federal employee’s wage to pay a delinquent debt. With the AWG process, these agencies do not require a court order to collect your wages. Federal agencies issue AWG orders to employers using Standard Form 329.

Private student loans

Private student loan wage garnishment follows a different process from federal wage garnishment.

For starters, private lenders need a court order before they can start skimming your wages—more on that in a second.

Like federal loans, private loans default after you’ve failed to make payments. But unlike federal loans, most private loans default after 120 days, though this time frame varies from lender to lender.

Next, private lenders assign your loan to an in-house collections department or send it to a debt collection agency. And finally, private lenders (or whoever holds your debt) must sue you, take you to court, and receive a court order before they can garnish your wages.

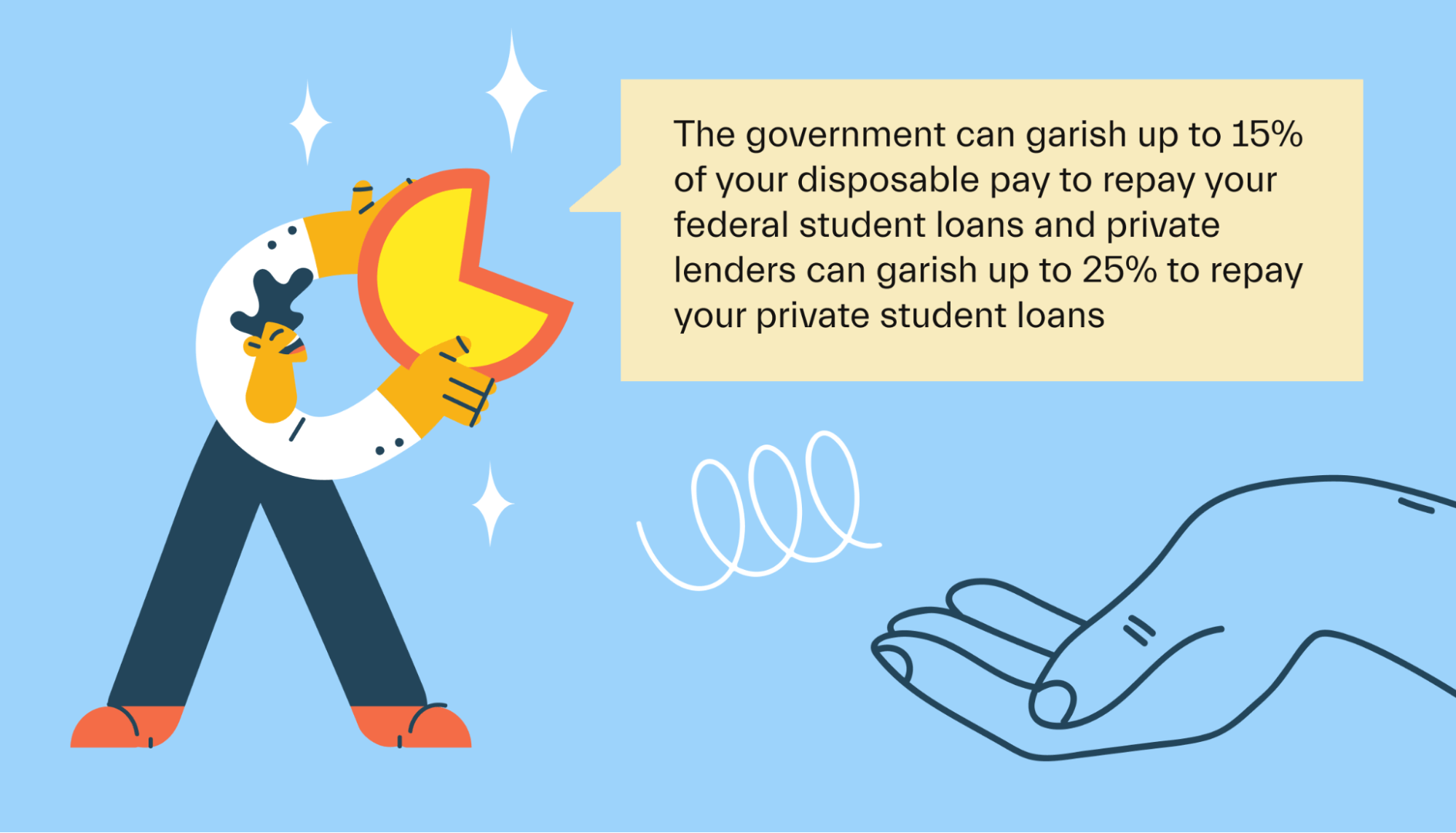

How much of your wage can be garnished?

Under the administrative wage garnishment process, the federal government can collect up to 15% of your disposable income until your loan is paid.

Private student loan lenders can garnish up to 25% of your disposable income but require a court order.

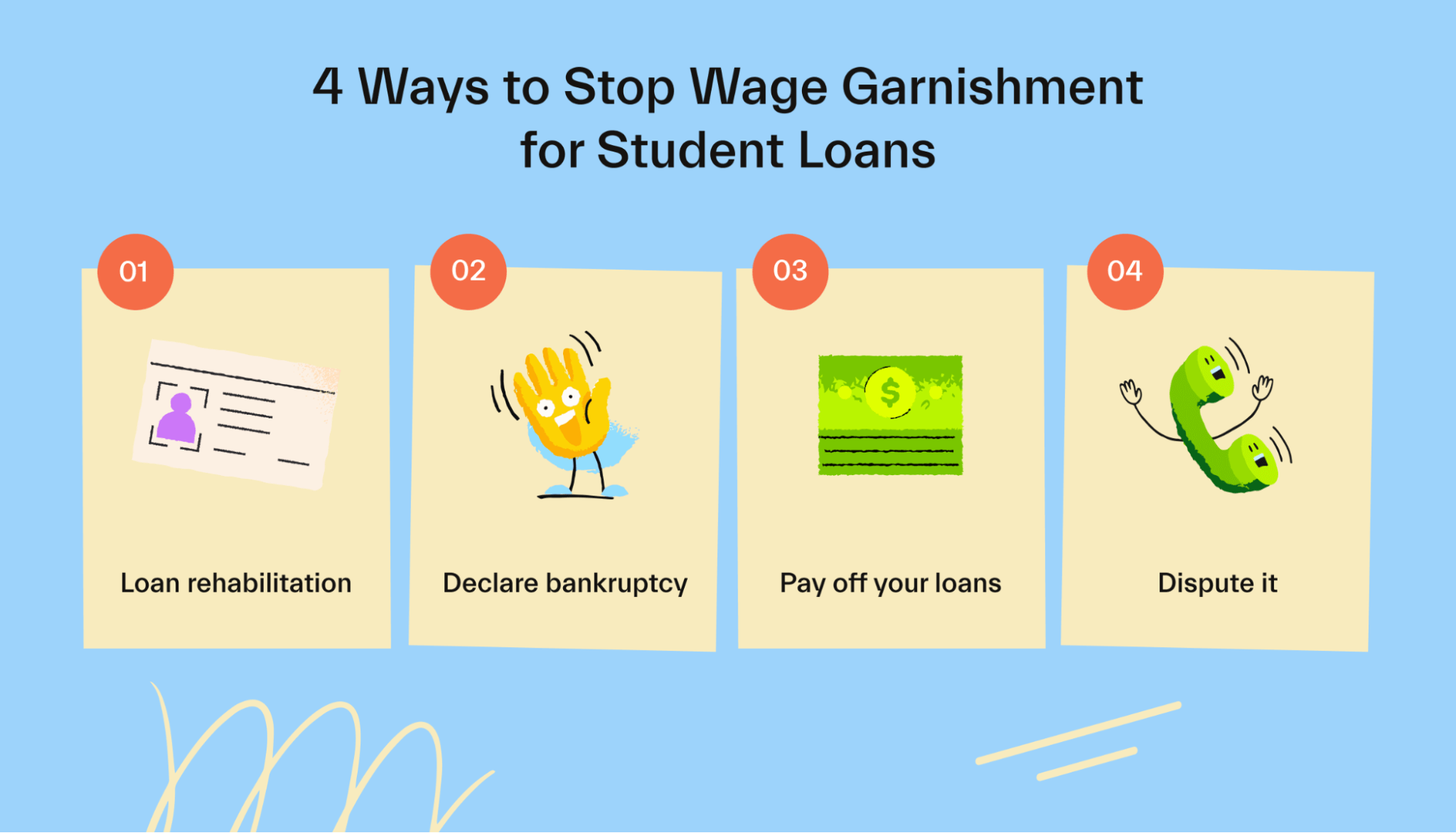

How to stop student loan wage garnishment once it’s started?

If your student loan is in default and your wages are already being garnished, don’t panic—there are ways to stop it.

Let’s explore a few tactics to stop wage garnishment and shoo away debt collectors from your paycheck.

Loan rehabilitation

Loan rehabilitation is an absolute life-saver if you’ve defaulted on your student debt. It stops wage garnishment and also removes your loan’s default status from your credit report. Not bad, right?

However, loan rehab is a one-time lifeline, so don’t agree to it unless you’re 100% sure you can meet the terms.

Here’s how to enroll in loan rehabilitation for federal student loans:

Contact your loan holder to see if you’re eligible

If you’re eligible, your loan holder will request your latest tax returns

Your loan holder calculates a monthly payment equal to 15% of your discretionary income

If you agree to make 9 consecutive monthly payments in 10 months, you’re enrolled in the loan rehabilitation program

Unfortunately, most private lenders don’t offer a 9-month payment loan rehabilitation option—if they even offer rehabilitation at all. So if you’ve defaulted on your private loans, reach out to your lender and see what payment assistance programs they provide.

Declare bankruptcy

Filing for bankruptcy halts wage garnishment while your case is open. But be warned, declaring bankruptcy—and proving your severe financial hardship to the court—is a Herculean trial.

Yes, bankruptcy is stressful. But if your financial hardships hinder your quality of life and wage garnishment is making it worse, bankruptcy can help soften the blow.

If you’re considering bankruptcy, chat with a student loan lawyer and see if it’s a viable option.

Pay off your loans in full

Paying off your student loans completely will immediately stop wage garnishment. Of course, this is far easier said than done. If you have the money to pay off your debt, kudos to you! If not, don’t worry—you still have options.

Dispute the wage garnishment and request a hearing

If you receive a wage garnishment notice from the federal government, you have the right to dispute the notice and request a hearing, in writing, within 30 days.

Technically, you can’t request a hearing after wage garnishment starts. But because it first requires that you default on your loans and receive a notice, it’s a bit of a gray area.

We’ll cover the specifics of garnishment disputes and hearings in a few minutes. The important thing to know is that you can challenge a garnishment notice, but you only have a narrow window to make it happen.

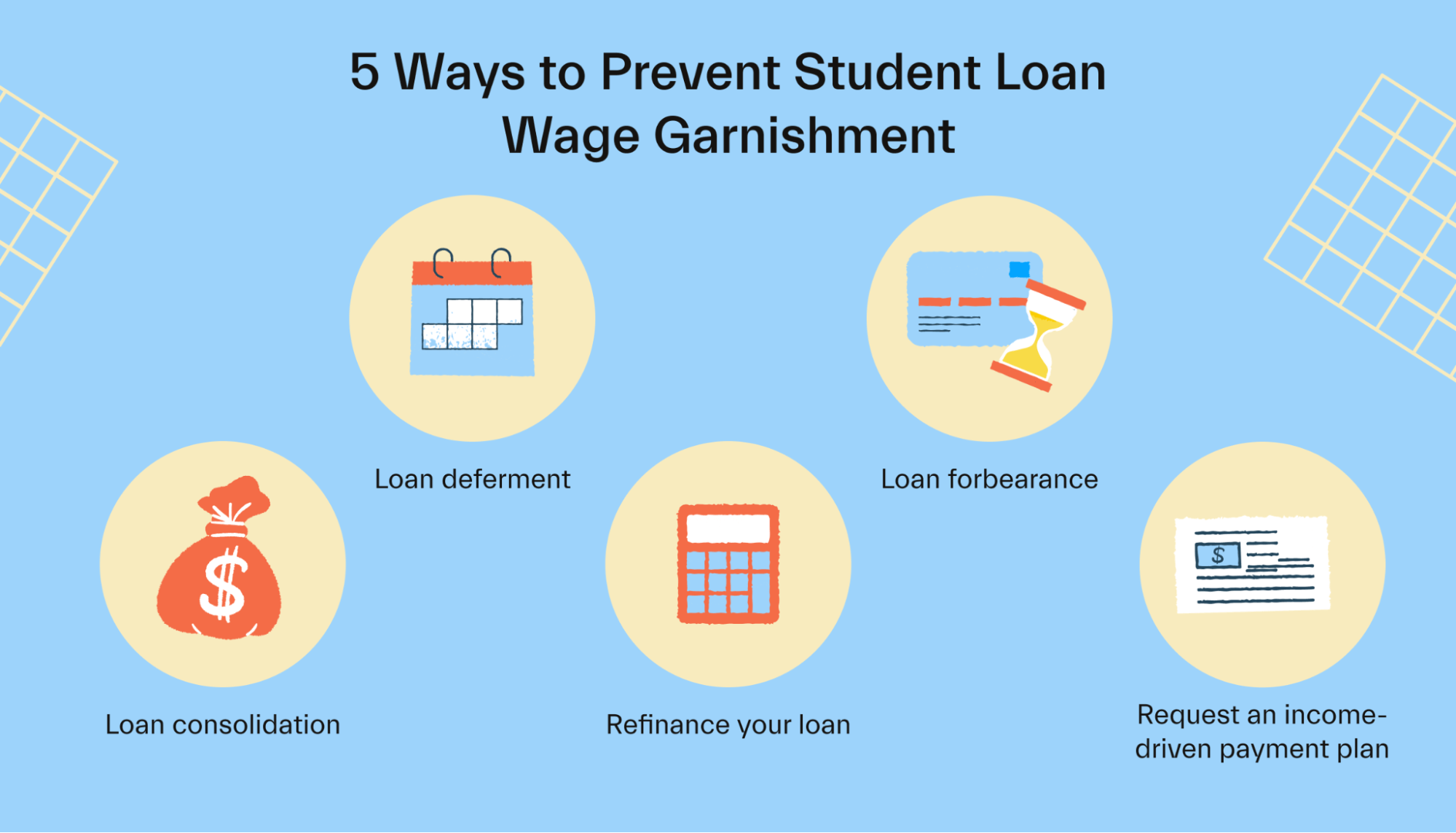

5 ways to prevent student loan wage garnishment

1. Loan consolidation

Loan consolidation takes multiple loans and combines them into one big loan with a fixed interest rate. This way, you only need to manage one payment instead of juggling several simultaneously.

You can consolidate your federal loans into a Direct Consolidated Loan at no extra cost. Private lenders, however, may charge a fee—if they even offer loan consolidation.

The bottom line is that loan consolidation makes it easier to manage your debt and keep it in good standing. And the icing on the cake is that you’ll likely secure a better overall interest rate by consolidating your loans, saving you a ton of money over your repayment period.

2. Loan deferment

A loan deferment is like putting your payments on pause. If you have federal student loans, you may be eligible for a deferment if you meet approved conditions, like:

You’re undergoing cancer treatment.

You’re facing economic hardship.

You’ve been accepted into a graduate fellowship program.

You’re enrolled in school and have at least a 50% course load.

You’re on active military duty.

You’ve been involuntarily unemployed.

Private lenders aren’t required to offer loan deferment programs but some do for exceptional cases, like the reasons listed above.

Despite what you may have heard about loan deferment, certain federal loans still accrue interest when deferred. These loans are listed below:

Direct Unsubsidized Loans

Unsubsidized Stafford Loans

Direct PLUS Loans

Direct Consolidated Loans

The unsubsidized portion of FFEL consolidated loans

Similarly, private loans will likely accrue interest during a deferment, but terms and conditions vary.

Remember deferment is only temporary. But if life’s circumstances or your financial struggles have you worried about defaulting on your loans and having your wages withheld, you have the option to hit the pause button.

3. Loan forbearance

Like deferment, forbearance lets you stop paying your loans temporarily, usually for 12 months. Interest still accrues on your loans, but forbearance is an option if you need the relief.

Qualifying for a forbearance on your federal loans requires similar conditions as deferment, such as:

You’re experiencing financial hardships.

You’ve been hit with unexpected medical expenses.

You’ve lost your job.

Most private lenders also allow borrowers to request a forbearance. But, again, the exact terms and eligibility requirements vary by lender.

Even though forbearance is temporary, it’s a handy strategy for preventing loan default and having your wages garnished, so don’t be shy about applying for a forbearance program.

4. Refinance at a cheaper rate

How does a cheaper interest rate on your loans sound? Well, that's precisely the goal when you refinance your student loans.

Refinancing means trading in your old loans for new ones with better terms. These terms may include a cheaper interest rate, a longer repayment period, or both. Either option helps lower your monthly payment, making it easier to manage your student debt and avoid defaulting on your loans.

Like private loans, federal student loans can be refinanced with a private lender. But if you do refinance your federal loans, you’ll lose all the perks and protections that come with federal student loans, like deferment, forbearance, and income-driven repayment programs (more on that next).

5. Request an income-driven repayment plan

Federal income-driven repayment (IDR) plans offer you a more affordable monthly student loan payment but come with a much longer repayment period.

With an IDR plan, monthly payments are based on a percentage of what you earn—usually 10–20% of your discretionary income.

Most federal student loans qualify for at least 1 of 4 income-driven repayment plans:

Revised Pay As You Earn Repayment Plan (REPAYE Plan)

Pay As You Earn Repayment Plan (PAYE Plan)

Income-Based Repayment Plan (IBR Plan)

Income-Contingent Repayment Plan (ICR Plan)

Now, income-driven repayment plans extend your repayment period to 20–25 years, meaning you’ll pay a lot more in interest over time. But following that repayment period, any remaining balance on your loans is forgiven.

Private student loan providers may offer income-driven or voluntary repayment programs, but the repayment periods won’t be as generous. They’ll also expect the balance to be paid in full when the repayment period ends.

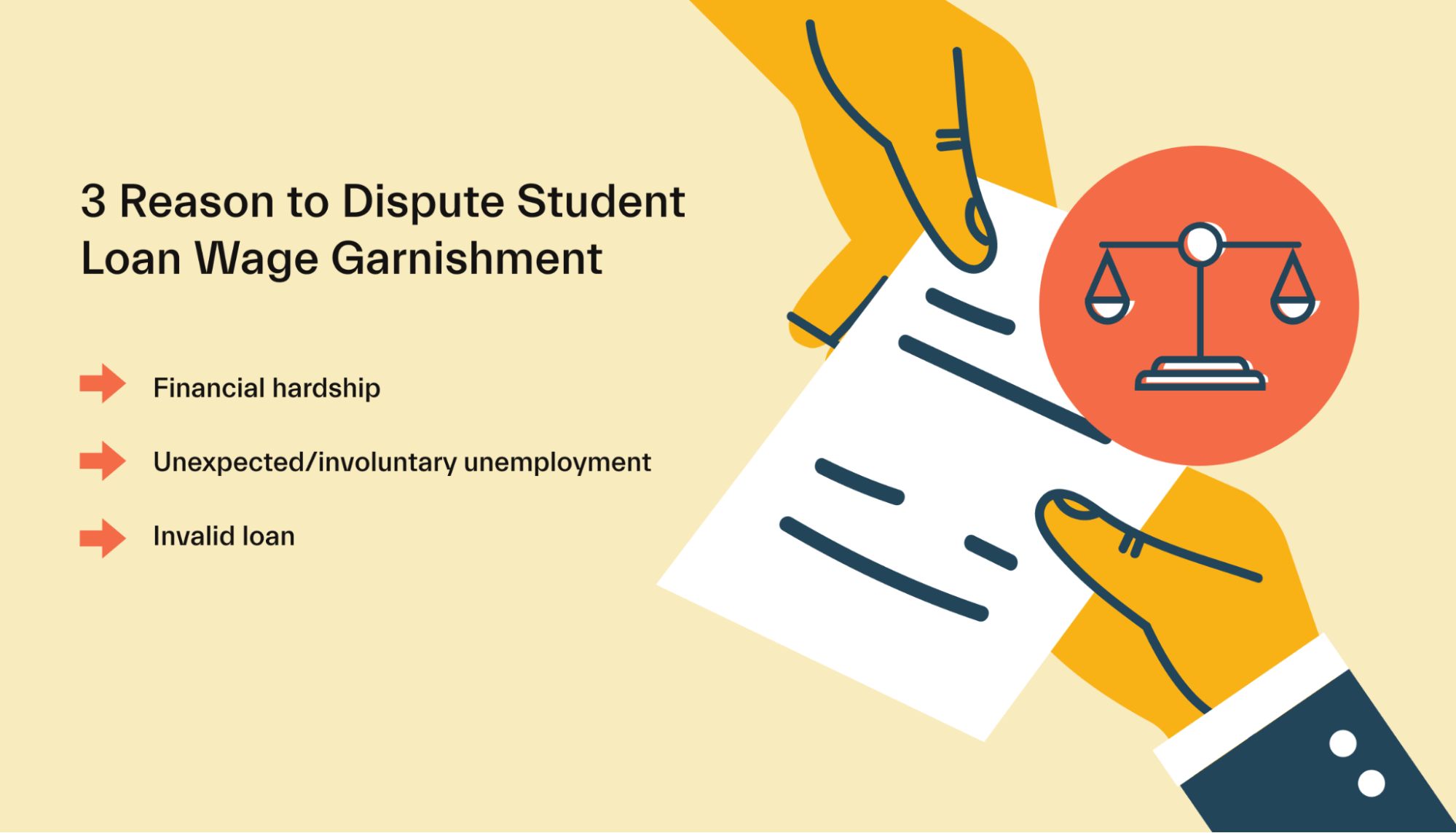

When (and how) to dispute wage garnishment

Just because you’ve been served a wage garnishment notice doesn’t mean you can’t fight it. Below we’ll review valid reasons for disputing a wage garnishment and, following that, walk you through how you can request a hearing.

Reasons for disputing wage garnishment

You have the right to dispute a federal student loan wage garnishment and request a hearing if:

Wage garnishment will cause extreme financial hardship, such that you can’t keep a minimum standard of living.

You’ve been employed for less than 12 months following a period of involuntary unemployment.

You believe the loan is invalid for whatever reason (for example, you think your balance has been miscalculated or that the loan isn’t yours).

Remember, these conditions only apply to federal student loans. Disputing private student loan wage garnishment is a different story. With private loan disputes, you’ll likely end up in court and must prove to a judge that you can’t pay your student loans and that wage garnishment would ruin you financially.

How to request a garnishment dispute hearing

After the Department of Education sends your notice of wage garnishment, you’ll have 30 days to request a hearing in writing.

After receiving your request, your loan holder will schedule the hearing. Meanwhile, you’ll need to collect proof that supports your garnishment dispute.

Your hearing may be held in person or over the phone. But in some cases, a formal hearing isn’t held at all. Instead, your loan holder simply reviews your proof-supporting documents to make their final decision.

Following the hearing, it takes about 60 days, starting from the time that your hearing request was received, to receive a decision about your wage garnishment.

The final decision on your garnishment dispute has 2 outcomes:

Your dispute was successful, and you’ll avoid wage garnishment for 12 months (or the percentage of your garnished wages will be reduced).

Your dispute was unsuccessful, and the government garnishes 15% of your wages.

Frequently Asked Questions

How can I get my student loan out of garnishment?

For federal student loans, your options include requesting a garnishment dispute hearing, applying for the loan rehabilitation program, declaring bankruptcy, or paying your loans in full.

For private student loans, contact your lender and ask if they offer any wage garnishment support programs or alternatives. If your lender doesn’t provide support, declaring bankruptcy or paying off your loans in full may be your only options.

Does garnishment affect your credit score?

Technically, defaulting on your student loans affects your credit score, not wage garnishment. So if your wages are being withheld, the damage to your credit score is already done.

How long can student loans be garnished?

Garnishment continues until your debt is paid. However, if you’re enrolled in an income-driven repayment plan, the unpaid balance on your federal loans is forgiven after 20–25 years.

Can student loans garnish your tax refund?

Yes. If you’ve defaulted on a federal loan, the federal government can garnish your income tax refund to help repay your debt.

Curb student loan wage garnishment (and keep Uncle Sam out of your paycheck)

Having your wages garnished to pay your student debt is like adding salt to a financial wound—it's defeating, embarrassing, and often doesn't do anything to address the real problem, the necessity of large student loans to fund study.

The best way to handle wage garnishment is to curb it altogether. But that's not always an option. So if you've been dealt a lousy hand and find yourself surrendering your money to the government before it hits your bank account, try some of the strategies outlined in this article.

The most important thing you can do to steer your finances is to stay educated. Keep up to date on the latest student debt developments and strategies with Mos.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you