Student loans •

October 28, 2022

Do student loans count as income?

Student loans don’t count as income when it comes to your income taxes, but that’s not the case for all types of federal financial aid.

If you’re like many other students heading off to college this year, then you’re probably financing at least some of your college costs with student loans.

But before borrowing money for college—or anything for that matter—it’s important to understand what you’re getting yourself into. And one question you may be asking yourself is...

"Do student loans count as income?"

The short answer is no, your student loans don’t usually count as income for tax purposes. But there’s a bit more that goes into it, and there are some types of financial aid that may count as taxable income that you should be aware of.

In this article, you’ll learn how financial aid is treated for purposes of income taxes and how your student loans might affect your taxes in the future.

Do student loans count as taxable income?

The good news is that for purposes of income taxes, your student loans don’t count as income. The reason they aren’t taxable income is that, unlike actual income, you’ll eventually have to pay them back.

That rule applies to any type of student loan you might borrow, whether you’re looking at federal loans or private loans. In fact, this same rule generally applies to any loan you borrow that you have to pay back.

In fact, not only do your student loans not count as income, they could actually help reduce your taxable income. However, student loan forgiveness (meaning when the federal government cancels your loans) does count as taxable income and can result in a large tax bill.

Don’t worry, we’ll dive into those two situations later.

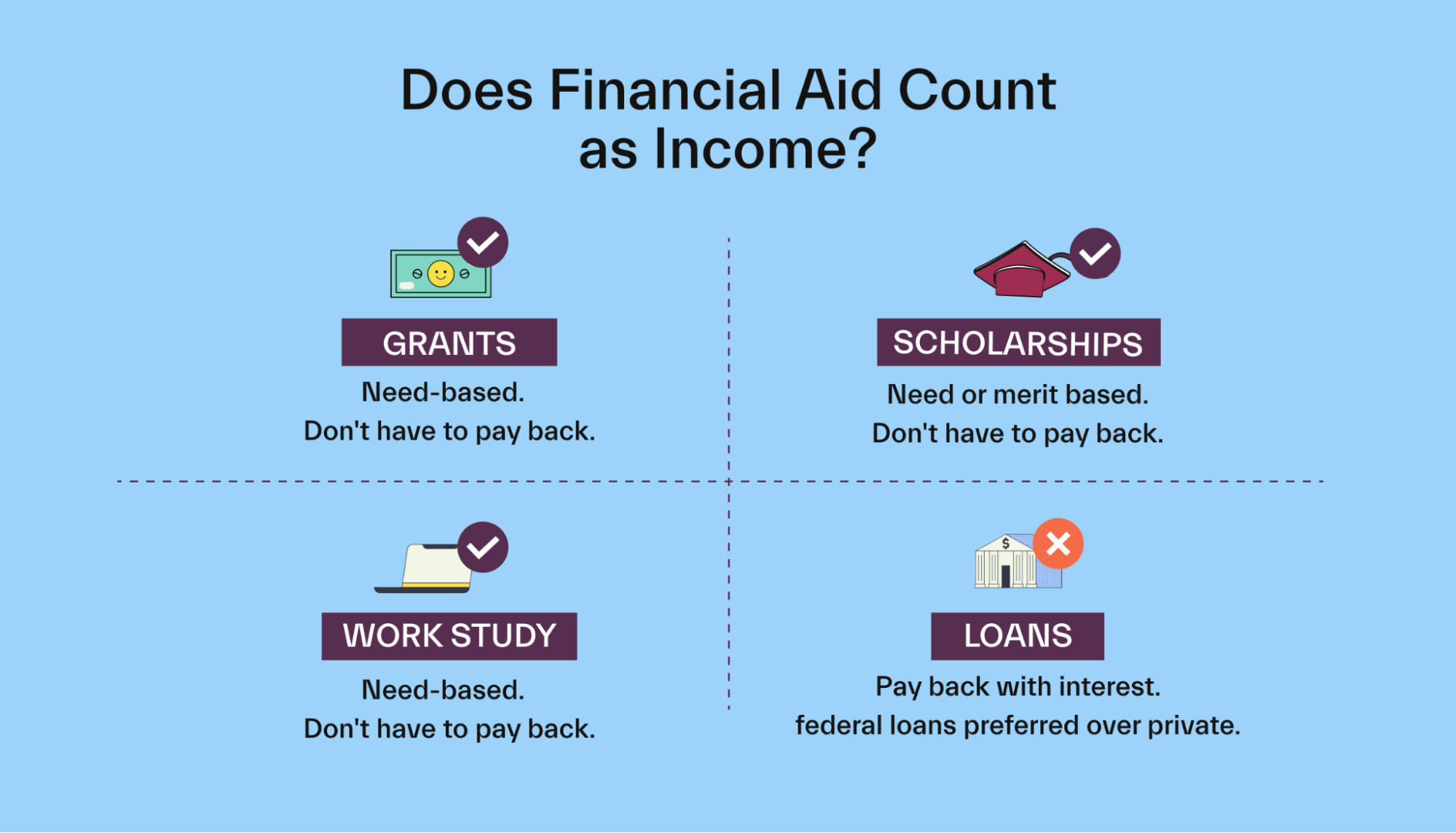

How other forms of financial aid affect your income

Alright, so we know that student loans don’t count as taxable income. But what about other types of financial aid?

It turns out that some types of financial aid are likely to count as income, so be sure you understand what to expect on your tax bill.

Let’s talk about the two other primary types of financial aid: work-study and grants / scholarships.

Work-study jobs

Work-study is a type of financial aid from the federal government where you get the opportunity to work on campus to earn money to help pay for school. Work-study is available part-time to full-time students or full-time to part-time students.

As with other types of income you earn at a job, the federal and (usually) state government expects you to report your work-study income on your tax return and pay income taxes on it.

The amount of tax you'll pay depends on the amount of work-study income you earn and the tax bracket you fall into as a result. If work-study is your only source of income for the year, then you may not have to pay much (or any) taxes.

If you earned work-study income, you should receive a W-2 form at the end of the year and will report that income on your 1040 form (the standard individual income tax return form).

Grants and scholarships

In general, the money you get from grants and scholarships isn’t subject to income taxes so long as you meet these conditions:

You’re a candidate for a degree at a school with a regular faculty, curriculum, and enrolled body of students.

You use your grants and scholarships to pay for tuition, fees, books, supplies, and equipment required for your classes.

However, grants and scholarships could be taxable income if...

You use the money for incidental expenses like room and board, travel, and equipment that isn’t required for your classes.

You receive the money as a payment for teaching, research, or other services that are a condition of receiving the scholarship or grant.

So long as you keep within those lines, you'll be fine.

What about employer tuition assistance?

While employer tuition assistance isn’t a type of federal financial aid, it is a type of financial assistance that many students get when they’re paying for college. Tuition assistance is a benefit that some companies offer in which they contribute to an employee’s tuition.

The good news is that the first $5,250 of educational assistance you get from your employer each year can be excluded from your taxable income.

In other words, it doesn’t show up as income on your W-2 form, and you don’t have to include it on your federal tax return or pay taxes on it.

If your employer offers more than $5,250 of educational assistance, then you’ll have to pay taxes on benefits over that amount.

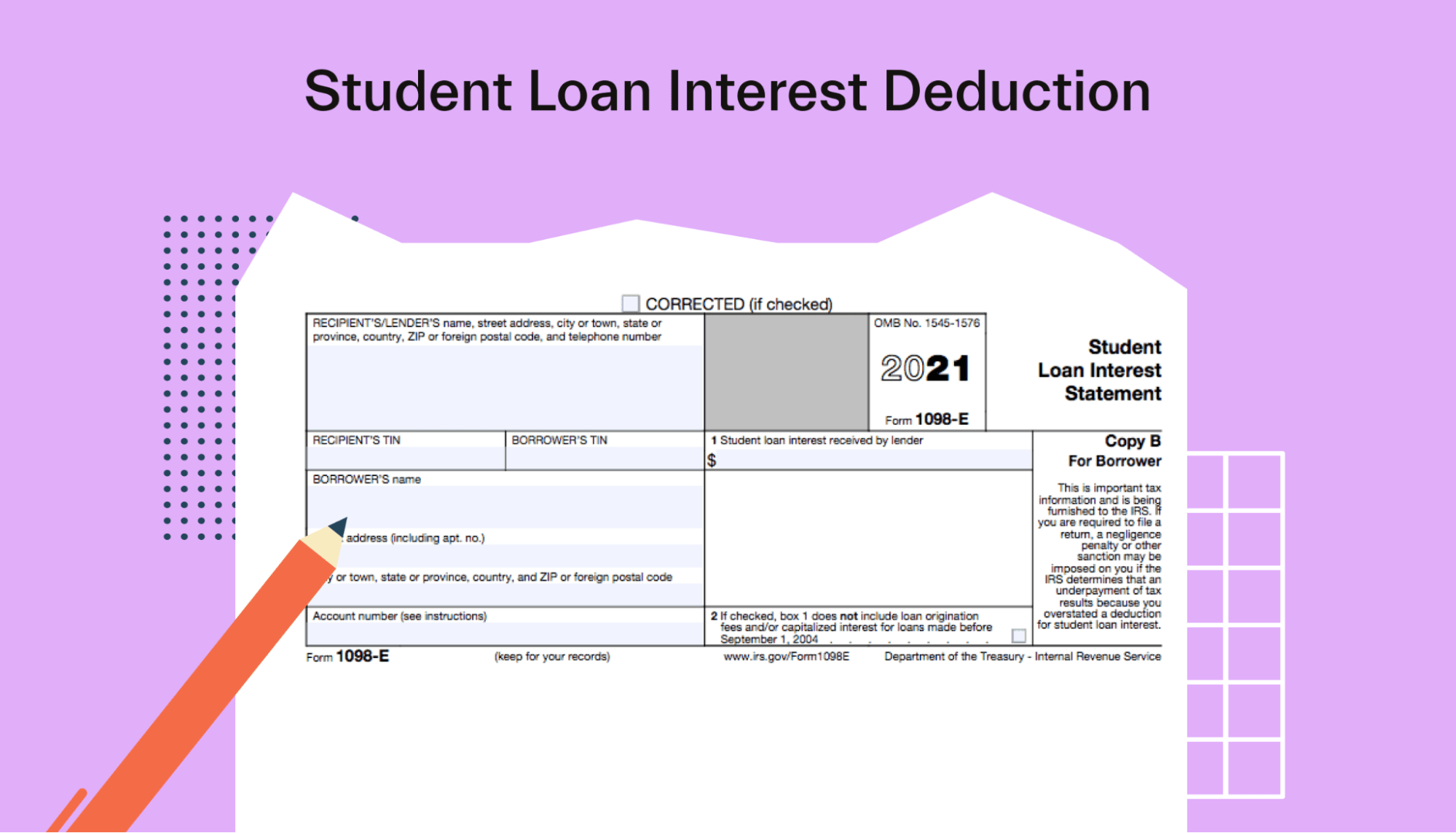

Claiming student loans on your taxes

Your loans can actually help to reduce your taxable income.

The federal government allows for a tax deduction for student loan interest you pay throughout the year. It counts on both required and voluntary prepaid interest payments, and you can deduct up to $2,500.

It might not seem like much, but it could increase your tax refund by several hundred dollars depending on your tax bracket.

For example, if you’re in the 12% tax bracket, the deduction could save you $300. If you’re in the 24% tax bracket, it’ll be a savings of $600.

Another perk of the student loan interest deduction is that it’s what’s known as an ‘above-the-line’ deduction, meaning it’s used to find your adjusted gross income. You can claim even if you claim the standard deduction and don’t itemize your deductions.

It’s worth noting that unless you start paying on your student loans early, this deduction isn’t likely to help you while you’re still in college. Instead, it’ll benefit you after you graduate and start making your required loan payment.

If this is all a bit more confusing than you'd anticipated, you can get expert advice from a Mos advisor.

Student loans on credit card and loan applications?

You might actually be able to count your student loan money as income when you're looking to qualify for a loan or credit card.

However, you can’t count the money that goes directly to the school to pay for your tuition. To count your student loan as income, you have to receive it directly. So if you get a refund from your school after they’ve used your loans to pay tuition and fees, that amount may be able to count as income.

Your student loans can also only count as income when you’re actually receiving them. You can’t use those same loans as income in future years.

Also, remember that while counting your student loans as income might help you get a credit card or loan, your student loan debt might count against you later on when trying to qualify.

When deciding whether to give you a credit card or loan, lenders use your debt-to-income ratio (DTI). It’s the percentage of your gross income that goes toward debt. So once you start making payments on your student loans, they’ll count toward your DTI.

With too high a DTI, you may not qualify for your loan or credit card or could end up paying a higher interest rate.

Does student loan forgiveness count as taxable income?

It’s also important to talk about the tax consequences of having your student loans forgiven.

There are programs in place to help certain students get their loans forgiven early. Some programs are specifically designed if you work in a certain field. But you may also be eligible for loan forgiveness after making payments on an income-based payment plan for a certain number of years.

First, let’s talk about student loan forgiveness based on your job. The most popular program for student loan forgiveness is Public Service Loan Forgiveness, which allows you to have your loan balance forgiven after 10 years of on-time payments (or 120 payments) while working in a public service role.

There’s also a Teacher Loan Forgiveness Program, which allows teachers in low-income schools to have up to $17,500 of their loans forgiven after 5 years.

The Public Service Loan Forgiveness and Public Service Loan Forgiveness programs aren’t taxable, meaning the forgiven balance doesn’t count as taxable income.

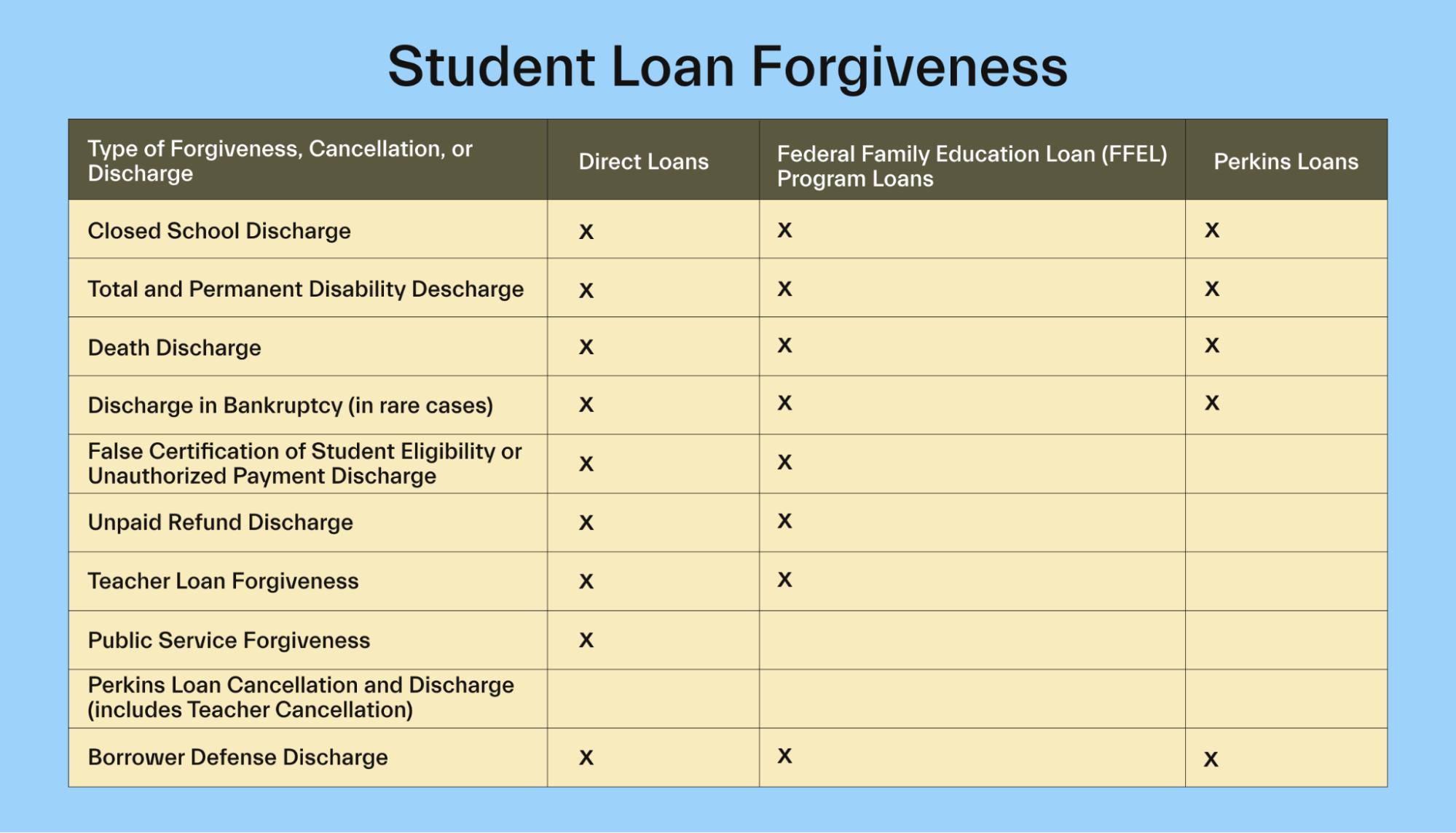

But there are plenty of other ways to have your loans forgiven, including:

Closed school discharge for schools that close while you’re enrolled or soon after you leave

Total and permanent disability discharge

Discharge due to death of a borrower or death of the student if a parent took out a PLUS loan on their behalf

Discharge in bankruptcy, which is extremely rare

Borrower defense to repayment if the school misled you or engaged in misconduct

False certification discharge if the school falsely certified your eligibility for a loan

Unpaid refund discharge if you withdraw from school and the school doesn’t return your loan funds to the loan servicer

Finally, if you use an income-based repayment plan for your federal student loan, the government will forgive your remaining after the full payment period (either 20 or 25 years). This rule applies to:

Revised Pay As You Earn Repayment Plan (REPAYE Plan)

Pay As You Earn Repayment Plan (PAYE)

Income-Based Repayment Plan (IBR)

Income-Contingent Repayment Plan (ICR)

It’s important to note that loan forgiveness other than that for public service workers and teachers normally counts as taxable income, and you’ll have to pay the taxes on it for the tax year in which it’s forgiven.

But as one of the many measures in place to help students during COVID-19, student loan forgiveness is tax-free for everyone through 2025. This rule applies to the expanded student loan forgiveness that’s happened under President Biden’s administration.

Final thoughts

Don’t worry—you won’t have to pay taxes on the money you receive from your student loans. And in most cases, your grants and scholarships won’t count as taxable income, either.

But there are exceptions to these rules.

For example, if you spend your grant and scholarships money on something that’s not an education expense, then it may be taxable. Similarly, if your student loans are forgiven down the road, you may pay taxes on the amount that was forgiven. Be sure to consult a financial aid specialist for questions.

Need help completing your FAFSA and finding scholarships to make sure you get all the aid you’re eligible for? Explore Mos memberships today.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you